Merchant cash advance information includes getting low rate cash advances, the best renewal terms, and how to get out of a merchant cash advance if they are causing your small business cash flow problems. Excellent options are available for business owners with a felony or misdemeanor in their background.

0:00 Introduction 0:18 How much are the Daily Payments 0:20 States that require 4 months statements 0:51 Monthly Deposit Requirements 1:10 Average Daily Balance Requirements 1:20 NSF and Overdraft Limits 1:34 Applying 1:45 Closing Documents Required 1:51 How Long to Funding 1:58 Repayment Problems; Video Description: How to get an MCA cash advance. Calculate affordability and payments. What is needed to close and what to do if you miss payments.

Looking for Tips on How to get an MCA Cash Advance? Complete the application above, Call us at 919-771-4177 or

use the Tips below! Information on how to calculate payments, how to get approved and avoid being declined. Read Tips on what to do before closing.

How to get an MCA Cash Advance

How to get an MCA Merchant Cash Advance

Supply: The last 4 months business bank statements

Tool: Desktop, laptop, tablet or phone

Step 1: How much are the Payments?

VIDEO CLIP below: See if your Business can afford a daily, weekly or monthly payment: 18 Seconds – 50 Seconds in Clip below.

Will Sanio, Smallbusinessloansdepot.com. Today’s Video: How to get an MCA Cash Advance. What could be your first Merchant Cash Advance.

Start the process anytime by tapping apply on the bottom right of this screen, or tapping on the end screen of this video, or the apply button on the webpage.

See if your business can afford a daily, weekly or monthly payment.

First, calculate an estimate of what your new daily Cash Advance Payment will be.

Let’s take an example:

Multiply a $10,000 offer amount times a 1.4 Rate Factor. There are 21 Payment Days most Months.

If your Offer Amount is for 7 Months, that’s 21 times 7 = 147 Payment Days.

Take the $14,000 Total Repay and Divide it by 147. That Equals $95.23 Per Payment Day

for Every $10,000.

MCA Total Cost Example

Step 2: Review your Company’s Cash Flow

VIDEO CLIP below: Review Company Cash Flow: CLIP: 80 Seconds – 93 Seconds in Clip below.

Look at the Total Deposits of each of your last 3 Months Business Checking Account Statements.

Some States require 4 Months Business checking account statements. Currently California, New York, Florida, Virginia and Utah.

The minimum total deposits into your Business Checking Account should be $5,000 a Month or more. The higher the Deposits, the more options are available. Especially beginning at $10,000 a month.

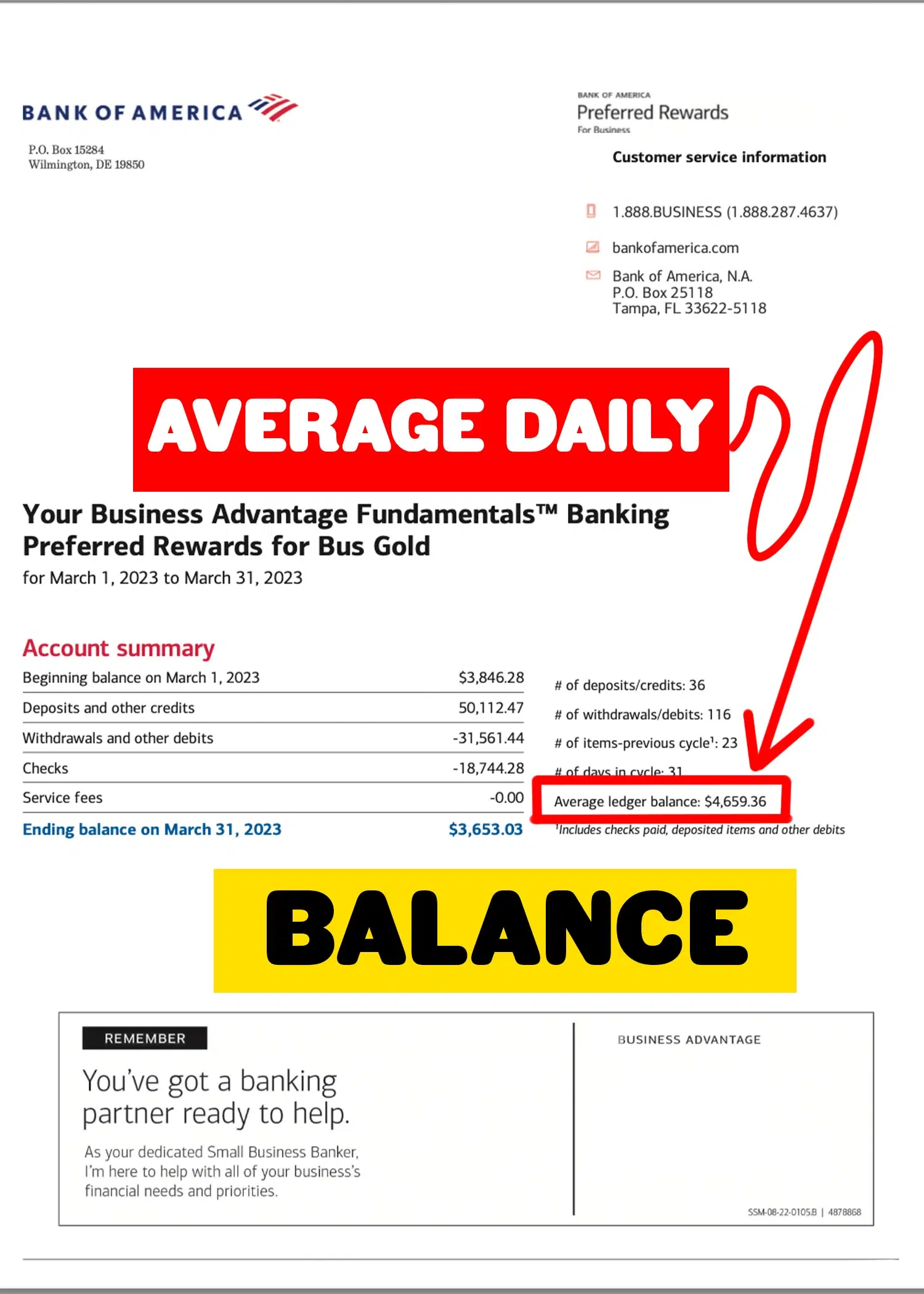

TIP: Average Daily Balance: That is the average balance per day for the Month. You want your Average Daily Balance to be at least $750, but better $1000 or higher.

TIP: Overdrafts or NSF’s. You should not have more than 5 to 7 Overdrafts or NSF’s in any 1 Month, or it is more likely you will be declined.

If you have more, it is better to wait until you get your next statement and those are gone.

What is the Average Daily Balance in your account?

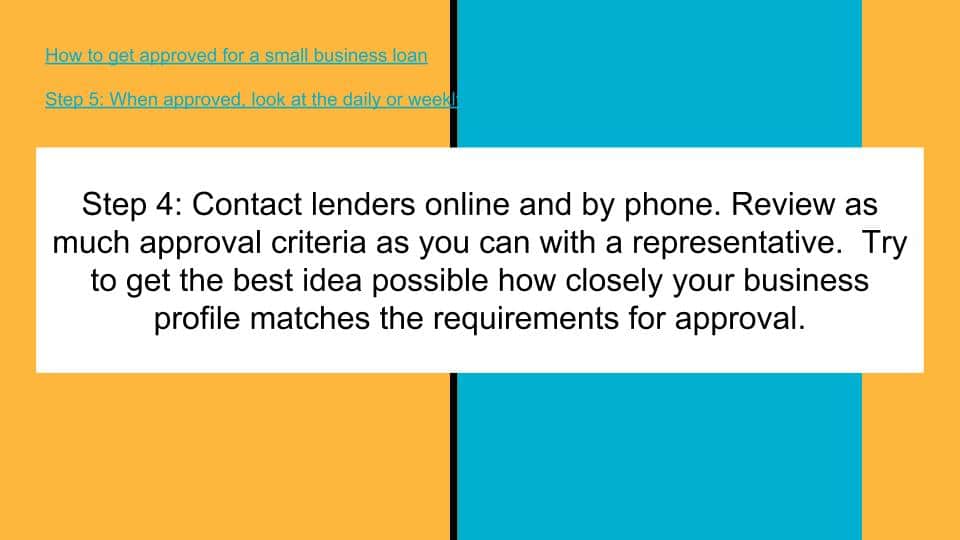

Step 3: Apply

VIDEO CLIP below: APPLY: CLIP: Seconds – Seconds in Clip below.

Find a Lender that fits your Business type and talk to a Representative before applying. That will help your business avoid unnecessary declines.

Next, Apply. If approved, request the closing docs. Get a Copy of your Driver’s License, Voided Business Check and Proof of Ownership.

Ready? Apply

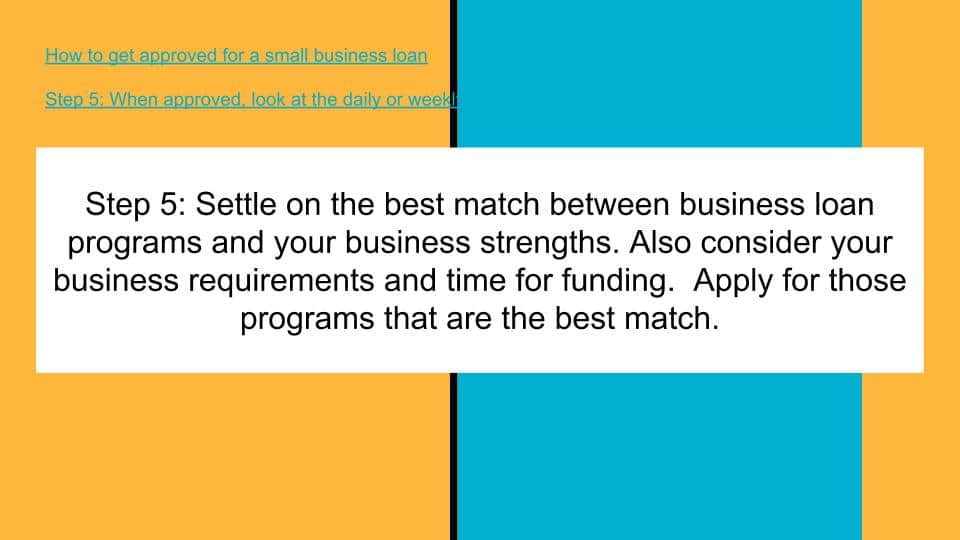

Step 4: Close

VIDEO CLIP below: CLOSING: CLIP: Seconds – Seconds in Clip below.

Next, close. Review the Contracts, and if you’re satisfied, complete the contracts and expect funding into your Account in 2 to 4 hours.

If you ever have repayment problems, call the Lender to discuss.

That will help your business keep it’s ability to borrow again in the future.

closing the transaction

Complete the application below or Call us at 919-771-4177.

0:00 Introduction

0:18 How much are the Daily Payments

0:20 States that require 4 months statements

0:51 Monthly Deposit Requirements

1:10 Average Daily Balance Requirements

1:20 NSF and Overdraft Limits

1:34 Applying

1:45 Closing Documents Required

1:51 How Long to Funding

1:58 Repayment Problems

How to Get an MCA Cash Advance

[ city street sounds ] Will Sanio, SmallBusinessLoansDepot.com

Today’s Video: How to get an MCA Cash Advance.

What could be your first Merchant Cash Advance.

Start the process anytime by Tapping apply on the Bottom right of this Screen,

or tapping on the end screen of this Video, or on the Apply Button on the Webpage.

See if your Business can afford a daily, weekly, or monthly payment.

First, calculate an estimate of what your new daily Cash Advance Payment will be.

Let’s take an example:

Multiply a $10,000 offer amount times a 1.4 Rate Factor. There are 21 Payment Days most Months.

If your Offer Amount is for 7 Months, that’s 21 times 7 = 147 Payment Days.

Take the $14,000 Total Repay and Divide it by 147. That Equals $95.23 Per Payment Day for Every $10,000.

Look at the Total Deposits of each of your last 3 Months Business Checking Account Statements.

Some States require 4 Months Business checking account statements.

[ ocean surf ] Currently California, New York, Florida, Virginia and Utah.

The minimum total deposits into your Business Checking Account should be $5,000 a Month or more. The higher the Deposits, the more options are available. Especially beginning at $10,000 a month.

Average Daily Balance: That is the average balance per day for the Month. [ teller counting cash ]

You want your Average Daily Balance to be at least $750, but better $1000 or higher.

Overdrafts or NSF’s. You should not have more than 5 to 7 Overdrafts or NSF’s in any 1 Month, or it is more likely you will be declined.

If you have more, it is better to wait until you get your next statement and those are gone.

Find a Lender that fits your Business type and talk to a Representative before applying. That will help your business avoid unnecessary declines.

Next, apply. If approved, request the closing docs. Get a Copy of your Driver’s License, Voided Business Check and Proof of Ownership.

Next, Close. Review the Contracts, and if you’re satisfied, complete the contracts and expect funding into your Account in 2 to 4 hours. [ clock ticking ]

If you ever have repayment problems, call the Lender to discuss.

That will help your business keep [ desert wind blowing ]

it’s ability to borrow again in the future. [ city street sounds ]

For additional help building your business, visit SCORE.org

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Watch Video above. Click or tap arrow to play. Call us at 919-771-4177 with any questions.

How to open a business checking account

How to Supply: EIN Letter, but not for a Sole Proprietorship using their SSN. Similarly, articles of Incorporation if Incorporating, or a License. Also Money to open checking Account, ID (Identification).

How to Tool: Desktop, laptop, tablet or also phone.

Estimated Cost: Approximately $100 minimum to start a checking account but the amount will depend on the Institution.

Step 1: Pick a Business Name

Choose a Business Name

Decide on what you will name your Business.

Choose a name that is relevant to your business type and easy to remember. Shorter business names that the public will easily identify can help build brand awareness.

Also decide if you will be 100% Owner or if there will be additional owners.

TIP: Avoid changing your business name in the future.

Step 2: Register Your Business

Go to the Secretary of State to Register your Business.

Go to the Secretary of State for your State. You can use this online tool, Searchsystems.net to Search. Find your State. Choose the company search option and do a name search to see if your chosen business name or similar name is available.

If it is available, decide on a Sole Proprietorship, Partnership, LLC or regular Corporation setup. An LLC is popular with small businesses for the legal protection it provides the owners.

Ask your County or City of they require any separate licenses.

Next, get an EIN number for your business through the IRS. This is needed for all businesses except Sole Proprietors that use their Social Security Number for taxes and tax returns.

Step 3: Gather all Documentation from Business Registration.

Gather all documents needed to register the business checking account.

Have ready your business name, Articles of Incorporation or Business License, and EIN Letter.

Step 4: Contact Institution and Open the Account.

Open your business bank account.

Go to the Bank to open the Business Account with all of your information: EIN Letter, Articles of Incorporation or Business License, and business name. If the bank is online, begin the process online.

TIP: All owners need to be present and show Identification. Acceptable identification is a valid Driver’s License or State ID Card or a Valid Passport.

Complete setup and enjoy the Account!

Conclusion: How to open a business checking account.

If you follow the steps above, then you can open a checking account for your company with no hassles.

If you have been using a personal checking account to run your business, then begin depositing funds into your new company checking account immediately.

Finally, you can use the cash flow in your new checking account to obtain services in the name of the business, such as bank statement loans, credit, credit card processing and other services.

Show Video Transcript Details

How to Open a Business Checking Account

How to open a business checking account.

Decide on what you will name your business. Shorter relevant names are easier to remember. Avoid changing your business name in the future.

Step 2: Register your Business. Go to the Secretary of State for your State.

You can use this online tool, https://publicrecords.searchsystems.net/ to Search. Find your State. Choose the Company Search Option and do a Name Search to see if your chosen Business Name, or similar name, is available. If it is available, decide on a Sole Proprietorship, Partnership, LLC or regular Corporation setup.

An LLC is popular with Small Businesses for the legal protection it provides it’s Owners. Purchase your Business Name. Ask your County, or City, if they require any separate Licenses.

Next, get an EIN Number for your Business through the IRS. This is needed for all Businesses except Sole Proprietorships that use their Social Security Number for Taxes and Tax Returns. Gather all Documentation from Business Registration. Have your Business Name, Articles of Incorporation, or Business License and EIN Letter ready.

Contact the Institution and Open the Account. Go to the Bank or Online to Open the Business Account with all of your Information: EIN Letter, Articles of Incorporation or Business License, and Business Name.

All Owners need to be available and show Identification. Acceptable Identification is a valid Driver’s License, or a valid Passport. Complete setup and enjoy the account.

To get a business loan, business credit or simple credit card processing for your business complete the contact form below.

This Article covers how to open a business checking account. Documents needed such as Tax ID number and getting a Secretary of State Listing is included.

To obtain needed services such as bank statement loans, asset based financing, or learn other self help for business issues including videos here. Watch just the Video Page here.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

List of the Top 9 Reasons why your MCA was declined

Top 9 Reasons Your MCA was Declined:

1. Affordability

This MCA decline reason means your company cannot handle the new payment without significant problems. This is often a decline

reason when your total monthly deposits are under $10,000 per month.

If you know you can manage the payment, then prove it! Provide your current bank statement, other accounts you may have, or tax return that shows you have the cash flow.

Make sure the investor isn’t using the lowest month to make their decision. Ask them to use the average of your deposit totals for your most recent 3 months.

This almost always happens when the business has cash flow problems during the current month.

The verification failed for either low deposit volume, overdrafts and NSF’s, or not enough individual deposits. It is usually some combination of these issues.

Ask specifically what they saw in the current Month that they don’t like.

Decide if this can improve enough to qualify in the next few days. If not, apply above to get another funding option.

4. Credit Score Too Low:

Some programs require a minimum credit score of 550, 600, or even 650.

Find out what score is required. If it is too high, apply for a program that will accept your credit score before you apply.

Ask the lender what minimum sales amounts are they looking for?

Also ask how much do you need to put into your account in the next week or two to qualify. By doing so, you may be able to qualify before the current month is over and not have to wait until the next month.

6. Recent Overdrafts or NSF’s:

Overdrafts or NSF’s in your checking account in the last 3 months were excessive, and why your MCA was declined.

Add up exactly how many Overdrafts and NSF’s you had. Ask the lender what the maximum is and how long before you will qualify.

7. Not Enough Deposits Per Month:

There were not enough individual deposits. Some funders require 5 or more each month.

Make more frequent smaller credits if possible.

Find a source that will accept the number per month you are now making until you can start making more. Ask in advance what their mimimum is.

8. Time in Business Too Short:

The time in business is not long enough through the Secretary of State or on your License.

Ask the funder how long they require. If you are within 30 days of the minimum, then ask for an exception.

If they refuse, then find a program that will accept how long you have been operating.

9. Background Check Failed:

A background check revealed something they didn’t like. When you get this MCA decline reason, learn more about a Business Loan with a background problem here.

Ask the MCA company specifically what the problem was, and if that matches what you know to be true.

Shop other MCA companies that have programs that accept your background issue before applying.

Unsecured financing has less risk. You do not need to offer collateral with a loan against your assets.

Up to 18 Month Term options for 600 and 1 Year in business and higher.

Get money against your cash flow again after payoff. Use it to get money more than once.

Programs for as low as $2,000.

Lower offers makes this a better option than regular title loans. No need to risk your vehicle or equipment for a small amount of money.

Need more general info on developing your business? Visit the SBA for resources

such as local assistance, business guides and business plans.

Conclusion: Why your MCA was Declined.

Your MCA was declined for one of these reasons listed above.

Take the actions listed and you can still get an approval offer and funding quickly!

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

So which Trailers Qualify to get a loan on a trailer?

Aluminum

ATV

Cargo

Custom

Dump

Enclosed and Open Car

Equipment

Gooseneck

Flat bed

Heavy Duty

Landscape Utility Trailers

LivestockTilt

Low Boy

Low Profile

Motorcycle

Refrigerated

Semi-Trailer

Tandem axel deckover and Dual Deck

Used Trailers

Utility

Racing

Vending

AND MORE!

Which Manufacturers? American Hauler, ATC, Big Tex, B Wise, Bri-Mar, CAM Superline, Car Mate, Cargo Pro, Carry On, Covered Wagon, Diamond Cargo, Homesteader, Master Tow, Premiere, Sno Pro, Sport Haven, US Cargo and more.

Bad credit and low scores down to 500 may still qualify.

So do I qualify? Do you own your Trailer outright and have a free and clear title ? Then you pre-qualify.

You don’t own it outright? Ask for our straight cash only program. Even when you still owe on your trailer! However, do you also have other equipment?

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Revenue is not equal, especially for your business. Lenders considering small business loans such as bank statement loans often look in detail at where sales came from in your business statements. They are looking to see if the revenue is from the operation of your business, or not.

What if your business has been denied because the lender did not accept a large part of your business sales?

Then Apply below for programs that count the maximum amount of your sales and deposits instead of deducting them and declining your business!

What isn’t business revenue: Types of Non Business Revenue

4 Main types of true Business Revenue that lenders accept.

1. Income from Sales to Customers and Vendors:

Revenue from the normal sales your business has is the most preferred and accepted income any business can have. Your business model is succeeding and can repay debt.

2. Income from Affiliate Partners.

Some businesses have affiliate relationships. Affiliate partners secure customers on behalf of another business. This income may come from the affiliate partners rather than those customers directly, but it is still valid receipts.

3. Money from Collections

Many businesses have delinquent accounts they collect on. Collection receipts are valid business income, even if they are from charged off accounts.

4. Money from the sale of business assets

When a business sells hard assets such as commercial real estate, business equipment or vehicles, it is considered business revenue and should be counted that way by lenders.

This includes soft assets such as proprietary software, intellectual property and patents. Any of these can have great value and be sold for significant amounts. When this happens, it is counted towards business sales and included in the annual income of the business.

Windfall from court decisions or judgements

Monies from court decisions or judgements is a grey area when it comes to lenders considering this as revenue for a business. Most will give this credit as true income from the business. Money from successful court litigation is considered monies that are truly owed to the business.

However, it is still a large one time event that will not be repeated. That makes it considerably different than money from sales which does constantly repeat, such as from a retail store.

What isn’t Business Revenue?

Transfers between business accounts or from other accounts

Transfers between accounts are not revenue for the business. The lender analyzes them to answer the following questions:

Was the transfer from another business account of the same business? If so, what has been the recent cash flow of that other account?

Savings Accounts:

Savings account transfers into a business checking account are not business income received by a business.

Personal Accounts:

Transfers from any personal account into a business accounts will not be considered business sales. Claims that they are must be documented and proven to the lender.

Business Loan Proceeds

Loan Proceeds are NOT considered business income. Money that comes from lenders cannot be added to the gross receipts of the business. It did not come from sales, so it is not business income.

Tax Refunds

Tax refunds are not part of business sales. Money back from the IRS is usually from taxes paid for previous sales, so the income has already been counted.

Rebates

Rebates is money a business gets back from an old purchase. It shows in the deposit section of a business checking account statement. Money had to be spent in the first place to get the rebate or refund and will not be counted.

FAQ on Business Vs Non Business revenue.

What is non business revenue ?

It is money that is not earned by the business from sales, sale of business assets, collections or the regular operation of the business.

Why is the lender not counting some of my business income?

The lender has decided that some of the money coming into your business is not consistent, or not the type they can count on to repay their loan, so they don’t count it.

How can the lender decline my business by not counting revenue that I earned?

The lender can count, or not count funds they see coming into your business for any reason. Their credit standards and criteria is not subject to law. It is based on their internal guidelines.

Conclusion

Some of your income may not be accepted as business income and may even be deducted resulting in a denial of your loan request.

Consider other lending programs when much of your revenues may be disputed as true business income. Contact us to match your business to programs that are not as strict in this type of review.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Was your business loan declined for a drop in mtd month to date revenue? Does your business have low monthly revenues such as less than $10,000 a month? Or Read the Full Article: Monthly Deposits under $10,000 a month. Review 7 ways to improve your numbers now and get approved as soon as possible by Applying below!

1. Understand your Statement. 2. Why were you declined for your MTD? 3. Total Deposits. 4. Average Daily Balance. 5. Number of Deposits. 6. Overdrafts or NSF’s. 7. What can I do?

7 Ways to Fix a drop in deposits and get approved ASAP!

1. What do lenders do with that Statement?

The statement is used to review your cash flow as of the beginning of the new banking cycle, or your most recent cycle date. Follow the link here to get a Month To Date (MTD) Statement in a PDF form.

2. Why were you declined for your Month To Date?

The statement used to decline your business will have lower than average deposits and be weaker overall than prior statements. Lenders ask for recent statements when applying and do not usually ask for interim information.

They only request it approaching the end of the month, or if the most recent statement was weaker than older ones before it. After the 20th, lenders may ask for the current cycle business account activity statement because a lot may have changed in those last 3 weeks.

Expect a request for the current statement when the last full statement was lower than average. Lenders are looking for trends in your business revenue, especially negative ones. Declines are not the end of the line. Consider the top decline reasons as well as other loan types such as a loan against equipment.

3. Total Deposits in the current month.

Your current monthly totals from business revenue is the most important information mca lenders review in the current statement cycle.

Prorate your revenues to estimate what the full numbers will be for the entire current 30 day cycle.

Example:

Your company had $35,000 in revenues from March 1st through March 12th. What is the company be expected to do for the full 30 days if they maintain the same revenue pace?

$35,000 X (31/12) = $90,417. To breakdown the math in simpler fashion, 31/12 = 2.58333. Since there are 31 days in March and it is the 12th of the month, the prorated fraction is 30/12. To express that as a % , 1/2.5833 = .387. This means that .387% of March has gone by.

Almost the same prorated amount is derived by dividing the $35,000 interim deposits instead of multiplying, as follows:

$35,000 % .387 =$90,439. The $22 difference is due to rounding.

4. Average Daily Balance.

Why is it important? When your account’s average daily balance is low, then payments are more likely to bounce.

Average balances below $1,000 and especially below $500 are red flags in credit review and will get your request declined fast.

Work hard to keep a minimum balance of $1,000 and higher because it increases your chances of approval.

Lower average daily balances in the current cycle are very closely looked at in the review process.

5. Number of Deposits.

At least 5 deposits per month are desired for cash advances. Other types of loans do not have this requirement, but more are better.

More usually means you have a higher number of customers which is considered a lower risk.

6. Overdrafts or NSF’s.

Overdrafts and NSF occurrences hurt the most in the current month. Many customers say they do not want to keep money in the account.

There is a difference between not keeping excess money in an account and having overdrafts because of it. Negative balances come from not having enough money and bad money management.

7. What can you do about a drop in month to date sales ?

Try to increase your deposit totals before the end of the cycle. Deposits made just prior to the end of the statement cycle instead of the first day or two of the next one help current numbers.

Don’t let your balances get too low causing returned payments that show as NSF or overdrafts.

Ask what you need to have for a chance at an offer now and you may be given target numbers. These will let you know if the numbers are achievable. If all else fails, consider a micro business loan.

Can my business be declined for low current month’s sales?

Your business can be declined for having a drop in revenue even in the current month that is less than a 30 day cycle.

Is there anything I can do to get approved now?

Following the cash flow strategy outlined here gives your business a chance of getting funding now. There is still be time to correct the numbers in the same statement cycle.

Are there options that do not look at the most current deposits?

There are asset based options with a monthly payment that usually do not look at the most current deposits. Those merit a close look for businesses that cannot wait for their cash flow to recover.

Conclusion

Declines for a business loan due to a drop in month to date revenues is a real possibility. Most lenders do not look closely at current 30 days, but some do.

Understanding what the threats to an approval are and the actions to take. Help your business steer clear of an unexpected turndown due to dropped revenues in the last 1 – 3 weeks.

Keeping a close eye on total and average balances and overdrafts during the current 30 day cycle can make the difference between an approval and a last minute decline.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

What are they? Payback months are the business bank statements for the same months 1 year ago. Lenders use these to help predict your company’s revenues in those months in the current year.

Apply below: for programs that increase approval amounts with strong payback months, but don’t lower offers with weak numbers a year ago.

4 Steps to understanding and handling this request

1. Understand Payback Months. 2. How to analyze your payback months statements . 3. Evaluate your requested amount. 4. Negotiation.

1. Understand Payback Months:

Lenders evaluating a loan request may ask for payback months statements for the previous year. This means they want the same months from 1 year ago that you would pay back any new loan this year. They use to check if you can afford an mca merchant cash advance.

Example #1:

Your business applies for a loan with a business lender. The lender is considering a 6 month loan for a bank statement loan to your business and asks you for payback months.

A 6 month loan will have a payback from March 2021 through August 2021. You will give the lender payback months bank statements from March 2020 through August 2020.

They want to see what your business revenues were for the same months last year. This forecasts what they expect your business to do in revenues during those same months this year.

Seasonal businesses are very susceptible to large swings in revenue during the year and can expect lenders to ask for bank statements from the previous year to compare.

2. How to analyze your payback months statements.

For 6 month loan requests, take the same 6 months from the previous year. Add up the total revenues and divide by 6.

Example:

From March through August of 2020, your company had a total of $120,000 in revenues. The average monthly revenues are $120,000 % 6 = $20,000 per month. Lenders offer 50% to 100% of average monthly revenues for most offers. $20,000 x .5 (50%)= $10,000. $20,000 x 1 (100%) = $20,000.

Offers should be $10,000 to $20,000, but may be less.

3. Evaluate your requested amount

Match your request closely with your business revenues. Do not ask for more than you can qualify for because it could cause an unnecessary decline or delay.

Ask for $20,000 if 50% of your company’s average monthly revenues = $20,000. Don’t ask for $100,000 unless you have assets to leverage for the request.

Do not state any amount and let the lender make an offer as an alternative. Lenders usually make the maximum offer regardless of your request.

4. Negotiate

Maybe your business qualifies for $20,000, but you need $25,000. Should you accept the $20,000? No! Ask for $25,000.

How? Get 2 or 3 offers from different lenders and leverage those offers with each to extract the maximum. Take the offer from 1 lender and show it to the other two.

This way, you are greatly increasing your chances of a better offer. Because 3 lenders have proof of a competing offer, they have more incentive to match and exceed their competitors.

Bank statements for the exact same months last year that lenders are considering a business loan to your company for this year.

Why am I being asked for Payback Months?

Lenders look your sales last year to help them understand if your business could make a new loan payment this year with the same sales.

Can they decline me for low revenue a year ago?

They may. The lender can decide that your business cannot afford the new payments with similar sales from last year. Explain why your sales will be higher for the same period this year, if so.

Conclusion

Understanding and reviewing your bank statement payback months from last year will pay off. Why? First of all, you can help avoid a decline by reviewing last year’s statements. If they are very low, go to another lender.

Also because you will have a better idea how much you qualify for, should ask for, and how to negotiate.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

You complied with the rules. Now you have been told you did not meet the conditions and your PPP loan was not forgiven.

Consider 4 ways below to deal with this along with other funding options if needed. Apply Below Now for Alternative Funding Solutions such as bank statement loans!

How to Deal a Repayment Demand when your PPP loan was not forgiven:

Was your ppp loan not forgiven?

1. First Look For Mistakes.

The government and large bureaucratic processes often make mistakes. Look through all of the guidelines and rules. Try to pinpoint how they came to their decision, and if it was correct.

Read their own official rules in detail since analysts make mistakes. But don’t just claim a mistake. Find their mistake, detail it, and also state why it does not apply to your case.

2. Appeal the Decision.

Appeal the decision regardless of whether you find a mistake or not. This also applies even when you are not likely to win. Many times having another representative review your case results in a different decision.

Find out the details of the appeals process and follow it precisely. Also followup during the process to make sure all your borrower rights are being met per legal requirements. Backed up government processors often cannot meet certain time requirements. Failure on their part may be a basis for a reversal in the decision.

Lack of proper documentation is the easiest problem to fix. Provide the proper payroll expenses, rent roll, utility and other statements. Submit any missing information as part of the appeal.

Incorrect Decision

Funds not used as intended is a common denial reason. As mentioned above, look for errors in their process. People do not find mistakes when they do not look, so review their response in detail.

Look for mistakes in the rational for why your ppp loan was not forgiven and then attack denials that are weak.

Did not fully understand

This basis for appeal is not a strong reason. However, it may be enough to a reversal of the decision in some cases.

3. Gather All Documentation to Support your Appeal.

Documentation is key, so gather and review all you information. Take a second look at your PPP expenses such as Payroll, Rent and Utilities.

Appeal Denied

Confirm whether appeals that are denied can also be appealed. Ask for time to respond to any denial in writing and also request an in person hearing.

Settlements

Make a formal counter offer in writing for a settlement and also document why your business cannot pay a forgivable debt. Provide cash flow statements such as tax returns, bank statements, Profit and Loss statements and Balance Sheet supporting your argument.

4. Find other Funding Alternatives

Look for alternative funding options to shore up cash flow shortfalls from unforgiven PPP business loans.

A business’ cash flow is impacted because they did not expect to have to repay a forgivable loan. Many other small business loans can be a good fit.

Asset based loans are also a great choice to assist with cash flow until the business adjusts to the partial repayment of their ppp loan.

FAQ: Why did they not forgive my ppp loan?

Why was my PPP loan not forgiven?

PPP loan forgiveness is not granted when you do not meet the usage conditions of the ppp loan stated in the contract. The most common reasons are incorrect use of funds and time deadlines for usage.

What can I do about it?

Carefully review the reason for the decline. Read the rules for ppp funds use and check for mistakes in the decision. Sometimes decisions are flawed or not clear cut.

How can I get the decision reversed?

Appeal the decision. Prepare all the documentation needed and submit a formal appeal.

Conclusion

A decline of forgiveness for your PPP loan may be a shock. Take action to challenge the decision that may lead to at least a partial reversal.

Since these loans can be for large amounts, it is worth the time to see if you can change the outcome. Look for mistakes in the process, prepare your paperwork and request an appeal.

MCA lenders look at percent of monthly revenue to decide if your business can afford a cash advance, and for how much.

Apply below for programs that offer the highest cash advance percentage of monthly revenue. This means the largest approval amounts because the highest percent of your business revenue is allowed for an mca.

This is about affordability, which is the #1 reason of the Top 9

Reasons why your MCA was declined.

Programs above offer the maximum approvals for mca’s as a percentage of your monthly business revenues.

How it Affects Your MCA.

Why it is Critical.

How it is Calculated.

Should You Care?

1. How it affects your MCA:

The percent of monthly revenues that an mca merchant cash advance can be is what drives the amount of the advance offer much more compared to other qualifiers.

It also tells you the maximum amount in advance that a specific lender allows for bank statement loans. Businesses that have an existing mca with a balance will therefore know how much more that lender can offer them.

Example:

An existing advance has a daily payment of $100 per day. The cash advance company you apply with allows businesses to have a maximum 30% of their monthly gross business revenue in cash advance payments.

Further, your business has monthly revenues of $25,000. So the total amount the lender allows your business in advance payments is $25,000 X .25 = $7,500 per month in payments. $7,500 per month % 21 days = $357 day.

An approval for 9 months should therefore render a maximum $48,000 offer by that lender.

While telling the mca company about advances with a few payments left seems like a risky thing to do, they will probably not include existing advance in their calculations.

Your business has average monthly deposits in the last 3 months of $50,000 per month. The lender you apply with allows the total monthly amount

you pay on MCA advances to be a maximum of 25% of your monthly revenues.

As a result, they calculate the maximum approval as follows:

$50,000 x .25 = $12,500 per month and there are 21 daily payments or

4 weekly payments per month. So using daily payments, $12,500 % 21 = $591 / daily payment at 5 business days per week.

Another critical step in the offer amount will be how long that lender will make an offer for. Longer terms result in higher offers, so a lender that offers a 9 month term can issue an approval of approximately $80,000.

This is because the math calculated to arrive at this approval amount is as follows:

$591 x 21 = $12,411 x 9 = $111,699, so a rate factor of 1.4 means that

$111,600 % 1.4 = $79,785.

3. Should you care?

You should care because it allows you to do 2 important things:

1. Calculate what percent of your monthly business revenue any mca will be before you apply. Also calculate whether you can afford the mca based the percent of monthly sales it totals. You will also better understand what your affordability limits are for this transaction and for all future borrowing.

2. Ask the lender before applying what the maximum is they allow. You may exceed the maximum and therefore do not need to apply. Also, the maximum amount they will approve you for may be too low. This will save you time, credit inquiries, and direct you to the best small business loan options.

FAQ on mca percent of monthly revenue for an advance.

What does percent of monthly revenue for an mca mean?

It means the maximum percent of your monthly business revenue

that can be allowed for a cash advance. Most lenders cap it between

20% and 30% of your monthly business revenue.

How do I know what my maximum approval will be for?

Take the average of your last 3 months total deposits. Multiply it times .25. This is the maximum amount per month many lenders allow you to pay for a cash advance.

What if I already have an advance ?

Calculate the maximum your business can afford per month. Deduct the monthly amount you already pay from that figure. That is the difference you can still afford on a new cash advance with many programs.

Conclusion

Calculating the percent of monthly revenues an mca will be as a percentage of your monthly business cash flow helps you make several important decisions.

You know in advance if you are applying with a lender that can help and approve you for the entire amount needed. You can ask lenders before you apply what their maximum percentage is and go to another lender if it is not high enough.

Another benefit is it helps you get the highest offers and saves maximum time by applying with the right funders.

For these reasons, know the maximum percentage of your business’s gross monthly revenue lenders generally will allow in mca cash advances. Also check back here on how to calculate approval and offer amounts needed to qualify for using the lenders maximum percentages allowed.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Learn the Top 4 ways to get a better business loan offer. Use this current program to max out the most favorable terms and conditions. Apply below now.

How to leverage a higher quality business loan offer.

Give your preferred lender a copy of any competing approval.

Ask for better terms.

Leverage your broader relationship with the lender.

Find out why the approval was not better.

Get better business loan offers now!

1. Show the lender a competing offer.

Give the funding source information on any other approvals you have to negotiate with them.

Example:

You are approved for $25,000 in bank statement funding, but you wanted a higher amount for more months. Your request was turned down.

However, you have existing offers from other funders. Send your preferred lender the actual approvals from another institution if it matches or beats theirs.

Effectiveness: This is often highly effective because it proves that you have multiple options. You have more negotiating power when other lenders know they are not your only choice. Providing documentation increases the pressure on your preferred lender to make concessions.

Rarely Done: Very few people think of showing one lender competing offers. The do not know that you have options from other investors. Stand out above other applicants and show competing offers.

Confidentiality: Is this confidential information? It is the same you gave the other lenders, so there isn’t anything confidential you are giving away. Your current lender already has the information, so it is not confidential.

The key conditions of the business loan offer are:

Amount: You can ask for approximately a 10% increase since some funding programs have the discretion to increase the approval by a small amount. Give a relevant reason why your business is asking for the higher amount.

Number of Months: The number of months often has some room for negotiation. Ask for a 3-6 month bump instead of 12.

Rates: Better rates are often hard to negotiate. The funding source will generally give you the rate that matches your risk profile. Negotiating rates may be easier when it is a brokered transaction and there are points or fees in the deal.

Check to see if there are different programs with the same funding source that would be a better fit. Doing so may give your business better terms automatically just by switching to another program.

Also ask the representative about features and benefits. There may be incentives and benefits in the existing approval that are already available just by asking for them.

3. Leverage any broader relationship with lender.

Applicants often have an existing relationship with the lender they apply with.

Deposit Relationship: Make sure the funding source considers any deposit accounts into their decision because automated programs skip this review in their processing.

Borrowing History: Any good previous borrowing history should factor into the approval decision.

4. Find out why the offer was not stronger.

Contact a loan officer and ask them why terms were not more favorable, such a higher loan amount, number of months and rate. Take a close look at those reasons and decide if you can overcome them right away rather than taking more time to fix them.

Example: Getting your credit score increased will take too long to help you right now. Getting updated financials showing your business in a stronger financial situation is faster and therefore could be used to get an improved business loan offer quickly.

FAQ: Frequently asked Questions on getting a superior business loan approval:

How can I get a better offer?

You may get better terms if you have multiple offers and show them to the lender you want. Tell them they need to beat the other offers in order for your business to close with them.

Will the Lender negotiate?

They are most likely to negotiate if they are given an incentive to do so. Applicants who prove they can close with another funding source and are prepared to do so will often get a negotiated closing.

What if I don’t get better terms from the lender?

Apply with other programs if you are likely to get multiple offers. After getting 2 other approvals, go back to the lender you want to close with and negotiate to get better terms.

Conclusion: Take advantage of easy ways to get better terms.

Most applicants do not push for better terms from lenders and as a result, sometimes miss easy chances to get a stronger deal.

Taking other approvals and asking your favorite lender to beat them always gives you a strong chance of getting concessions. Ask for better terms and use any existing and previous relationships when negotiating. You will probably greatly increase your chances of getting an improvement on the original approval!

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Having the right Business ownership percentage is very important for obtaining small business loans. If one person has less than 80%, they usually cannot close the loan by themselves. Many lenders want 100%.

Apply below for programs that allow less than 100% to complete funding.

100% Business ownership NOT required for financing.

100% is not needed.

Shareholders as low as 25% for some bank statement loan programs. Most options require at least 51% to 81%.

1 Owner can sign in many cases.

Remaining shareholders do not need to sign for some programs.

Top 7 Benefits:

1. Financing programs that fund with less than 100% ownership.

Get approved and also be able to close the loan with less than all the owners applying and signing on the note.

2. 1 owner may be able to close by themselves.

Another benefit is the other owners do not need to sign. Therefore, you don’t have to negotiate with them and convince them to sign on the loan.

3. 1 Shareholder may be able to make decisions.

You can make the decisions on the company loan even though you are only one of the shareholders for some options. Decide how much to borrow, for how long and any other options offered by the lender.

4. The other partners do not provide a personal guarantee.

The personal assets of the non signing partners are protected. Many are not spouses or family members and their assets are separate when applying.

The personal assets of other shareholders will not be at risk under the loan, which is significant. Others often hold Real Estate and other assets separately.

When there are several owners with similar shareholder percentages, it is difficult to complete many basic transactions such as sales with vendors, contracts and contract changes.

Shareholder percent of assets.

Assets that are in the company name are owned by all of the owners.

There is excellent business financing against vehicles with monthly payments. Carefully review how shareholders are specifically listed on all assets, including on titles for loans against vehicles.

Selling, negotiating, or transferring joint business assets

Assets in the company name with multiple owners must have the approval of all of them for any changes. Everyone must agree and sign for the sale, transfer and any loan against an asset.

Anyone excluded from the sale invalidates that sale.

Selling with multiple owners.

All must approve and sign any sales contract when the company is sold. One party cannot sell it alone.

Ownership control of Checking and savings accounts

Checking, savings and other commercial accounts can be opened without all owners. Authorized signer information is keep on file by financial institutions.

One signer also cannot remove another signer from the account. Other signers must agree to their own removal. If one owner wants to be on an account alone, they can open a business checking account with themselves as the only signer.

They should check what the banks’ rules are for making changes. Changes such as closing an account, withdrawing money are difficult later without specific documentation.

Changing stakeholder percentage.

Update the articles of incorporation or organization to increase or decrease these sipercentages. The articles may vary by state.

Many times, corporate articles do not list share percentages. Most articles list principals such as President, Vice president, CEO and officers. The lender does not have the breakdown.

A big reason businesses fail is disputes between owners, including who has the authority to make decisions and complete transactions. Including specific percentages and shares owned eliminates many future disputes. New corporations should include this information in their paperwork.

Use addendums and corporate change paperwork to add this information. Another option is to add a notarized corporate change resolution or additional information page. File these with the Secretary of State.

FAQ: Frequently asked Questions:

Do I need 100% ownership to get a business loan?

100% is not always needed to get a small business financing. Programs are available with percent ownership below 80% and as low as 25 in some cases.%.

Does my business partner have to sign if they don’t want to?

Partners do not have to sign when one has enough ownership. Ask the lender what is required for closing.

Can I remove my partner from the business to get a loan?

No, and you cannot remove your partner without their approval in general. Lenders do not want quick changes just to get the funding. Get approval from the funding source first before attempting this.

Conclusion: Business loans closed with one signer has major advantages

As described, one company shareholder with the authority to close a loan has many advantages. They can make all the decisions on their own. They do not have to discuss and get agreement from others, which is often a major hurdle. This includes financing and applying for working capital loans.

Choose financing that funds and closes with one owner. Find out the requirements from the lender and make changes to your company profile for insufficient shareholder percentage, if needed.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

There are several ways to reverse a business loan decline into an approval fast. A lot depends on the reasons. Some can be handled in days and you can change a denial into an approval with these easy fixes.

Apply below now for programs such as bank statement loans that specialize in dealing with common decline reasons.

Bureau scores that are too low are among the most common declines. Many people believe it takes years to improve their file and that they have to pay a credit repair agency to fix their negative reportings.

Incorrectly Reported Bureau Information:

Many times, information reported by the consumer reporting agency is incorrect. Review your report and look for inaccuracies. You can often get corrections and deletions updated within weeks. Once you have identified the incorrect trade line reports, you can dispute it yourself with the reporting agencies, or hire a credit repair agency.

You will have already done much of the work just by reviewing your file in detail. Doing the rest yourself lets you follow up faster and dispute it again if the reporting agency puts the same slow pay items back on your file.

Outdated Bureau Information

Sometimes outdated information hurts your scores. An old account may still be showing on your report that has been paid. A balance on a current account can be much higher on the bureau than the true balance. Some creditors do not report every month. Disputing or updating outdated trade lines in your file can often increase your bureau scores. Tell investors when you really owe less than what the bureau shows. That improves your ability to pay new debt.

Scores Too Low:

Often, your current scores are too low. Taking the actions above should increase your score because fewer derogatory and outdated items will be on your file. Your bureau scores will jump quickly and may trigger a reverse of a loan decline. Other funders may approve your company with higher scores as well.

2. Debt to Income ratio too high or cannot afford new payment.

Debt to income ratio is the percentage of fixed monthly debt divided by monthly gross income. This is often calculated as part of the credit review process.

For example: A borrower has monthly income of $5,000 and fixed obligations of $2,000. Their d/i ratio is $2,000 % $5,000 = 40%.

If a borrower’s percentage is too high, they may be rejected. Businesses with higher gross sales than others are likely to have more discretionary income with the exact same debt ratio. If you can afford the payment, then document your cash flow. Contact the lender and show them your company’s disposable income figures. Prove that you can make the payment and ask to appeal the denial.

3. Insufficient Cash Flow

Lenders may look at your overall cash flow. Many require a minimum amount of annual company sales to even be considered for financing. Many calculate the maximum loan or mca as a percent of your monthly revenue.

Funding sources that reject for this reason often do so in part on the most recent tax return figures. Your most recent business tax return is already dated. Provide a year to date YTD Profit & Loss statement and Balance Sheet when the current year is stronger than the previous one. Doing so may justify approving a request that originally did not pass the approval process.

If your current year is about the same as the previous, then you would need to figure out other debt or income information that could potentially reverse the denial. For example, large new customers that are new will increase revenues substantially.

4. Too many recent inquiries.

Denials from inquiries can happen if the owner(s) have recently been making purchases that require financing, or new services that require a credit check. Lenders have become more savvy at assessing these, but their automated reviews are not perfect and may not account for inquiries that should not be counted.

Many financing programs use a soft pull instead of a hard pull. However, some programs use a soft pull initially to make an offer but still do a hard pull later before closing.

If a lot of your inquiries are from shopping for consumer goods, or related to living expenses such as utilities, then document these. Contact the funding source and show them what the inquires were for, and they may re-consider their original decision.

5. Ownership percentage not enough.

Applicants must have at least 80% or higher ownership in the company to be able to close most financing on their own. Many lenders require a higher percentage such as 95%, and often full 100% ownership.

Discuss this with the other owners. 100% ownership is required for most financing so they may be required to sign. Your enterprise will eliminate itself from good options if one owner with less than 100% ownership wants to get funding on their own.

There are exceptions for owners with very strong credit and assets. Owners with bureaus over 700 and a strong personal financial statement may be offer a guarantee by themselves with less than 100% ownership. However, many investors will not consider any request with less than 100% of the owners applying, no matter how strong any one owner is.

6. Unacceptable or No Financial Statements or Tax Returns.

Some financing requires financial statements that the applicant does not have and is rejected as a result. This usually includes the most recent 2 to 3 years personal and business tax returns, current interim financial statements and bank statement payback months for the same repayment months the new financing will be for.

Gather and provide the missing items and request your application to be reconsidered.

In other cases, financial statements were not acceptable. This normally means the gross or net income was not high enough, or not enough the cover the new payment. A decline may result from just having one lower sales year out of the last three. They want to see steady or increasing business revenues annually or they will not approve the request.

Alternative Options: Look for other programs if this is required.

7. Recent Low Bank Balances or Overdrafts.

Even with a strong company and personal profile, recent low bank balances or overdrafts may be a source of rejection.

Your may need the cash because of a recent slow sales. Many lenders are not forgiving to recent slow cash flow and overdrafts. Applicants believe recent low sales is why they should be approved for funding. Funding sources believe low sales in the last quarter is why a borrower wont’ be able to pay and therefore don’t make the offer.

Alternative Option: Look for another lending program, or wait 30 to 60 days for your cash flow to rebound some, then apply. If you can wait, first ask if it will make a difference. Consider other sources when your request will not be reviewed again later.

Discuss your recent cash flow or overdraft issues in depth with the lender that rejected your business. They will tell you they will reconsider it, but are very unlikely to change their original decision to an approval. Many investors must consider all requests, whenever made. Talk to them about fixes to previous issues before re-applying.

FAQ: Frequently asked Questions on how to reverse a business loan decline fast:

How can a decline be reversed?

The reasons can very often be quickly corrected or improved by making relatively easy updates or changes, such as ownership percentage. Ask the lender if the changes you make may cause them to change their decision before you re-apply.

Can the decision be overturned into an approval fast?

Many changes can be made within days that allow a lender to reconsider the request. Other changes will take longer but may still be accomplished within 30 or 60 days.

What if I can’t wait?

If you do not have the time to make corrections, then the best approach is to consider another type of funding that will not give you the same negative result. Talk to other lenders in advance before applying.

Conclusion: Change a business loan decline into an approval

Do not believe that nothing can be done after your business does not get an offer. Reverse a business loan decline into an approval today. Having documentation, a strong rationale and persistence are key to turning a no into a yes.

Sometimes the wait may be weeks, but the result can be reversed in the end.

You will understanding what can be corrected and this is information to use in your favor to get the funding needed!

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

How to keep a lender from taking too much collateral:

Ask about collateral requirements.

Don’t offer all of your assets upfront.

Negotiate the requirements.

Negotiate lien releases during the loan.

1. Ask for all collateral requirements before you apply

Finding out during the loan process that collateral you don’t have is required is too late. Ask what is needed before you apply.

2. Don’t offer all of your Assets up front.

Do not voluntarily offer too much collateral at the beginning of the process. You may be required to provide a listing of what you own later. First give a general description or possibly a personal financial statement.

This prevents the lender from automatically taking all of your assets as security for the transaction. Don’t give them something valuable upfront they did not ask for. Use this as a negotiating chip. Compare their loan offer to the value of your assets. Calculate the loan to value, or LTV.

3. Negotiate the assets required

Many investors will automatically take as much as they can, even if it may not be required to cover their risk and exposure. Banks and the SBA do this commonly. Many will take 5 to 10 times as much collateral as they need just because they said they wanted it. This contradicts what is expected with ethical business loans, but is standing in traditional banking.

After you have gotten an approval, push the funding source to take only the security they need. They may refuse, but you should ask anyway. Calculate the dollar amount of the principal + interest. Figure out how much in assets they need to cover the debt and how much more they are requiring. Check if assets are jointly owned if you have less than 100% ownership percentage in the business.

If their request far exceeds what they need to protect themselves, then present them with your calculations and valuations. This will be your proof, best case, and put the most pressure on them to lower their requirements.

4. Negotiate a release of lien during pay down.

You pay down the balance during the term of the loan, beginning with the first payment. The balance usually goes down much faster than the value of the assets. Sometimes, asset values go up instead of down.

If multiple pieces of Real Estate are being held, then negotiate before closing. Try to get them to agree in writing to release pieces after the balance has been paid down enough to still cover their debt. A condition may be timely payments and no other violations of the contract on your part.

Another option is getting a lender to subordinate their debt . This may be required because the new funder may not want to take a lien position behind the others. If you want to close the transaction, then you can approach the existing lien holders and ask them subordinate their position. They will then need to complete a subordination agreement.

Equipment transactions can be handled the same way. Ask for agreement ahead of time that pieces of equipment will be released from the lien as the balance is paid down. It is tough to get this approved but make the request because late in the loan the balance will be low.

Since the balance will go down faster than the value of the collateral, remind them that their risk position gets better every month after closing.

FAQ: Keeping a Lender from taking too much Collateral:

What is too much collateral?

When lenders approve a loan and take much more collateral than they need to safely cover the balance if you default. Banks routinely take excessive security on their transactions.

Can the lender take as much collateral as they want?

Funding sources take as much collateral as they want or you are willing to give them. Do not offer all of your assets in advance without negotiating for less. How can I keep the lender from taking all my assets for the loan?

Find out program collateral requirements from the lender ahead of time. Negotiate the collateral terms right after an approval. This is when you have the most leverage to get changes.

Conclusion

Many lenders often ask for all the collateral you have available.

Most people and businesses believe they do not have any say, influence or choice in this decision. They do. The borrower may not get the lender to lower their collateral requirements much, but they sometimes have success. It depends on the source, the transaction, and how you negotiate.

Ask for reasonable concessions and justify your request. This may include calculations, valuations and other proof. You will get some of what you want more often than you think.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Loan to Value is the maximum percent of the value of an asset a lender will loan against. It is usually based on the retail sale value, but not always. Sometimes it is based on the Auction or Liquidation value.

For Example, if an asset, such as a house or piece of Equipment is worth $200,000 in the marketplace and the lender will loan a maximum of 75% Loan to Value, also known as LTV, then the maximum loan amount the lender will give is $150,000. This is because $200,000 X .75 = $150,000. better terms.

Consider 7 ways, detailed further below to maximize your borrowing strength.

1. Understand Loan To Value, also called LTV. 2. How to use the equity in your assets. 3. Negotiate. 4. Know the risk of loss. 5. Get the highest % funding against collateral. 6. How does credit affect the percentage? 7. How can an appraisal help?

Get the most out of your assets

7 ways to use loan to value to help get the money you want.

1. Loan to value: How it works:

LTV is the amount a lender offers as a percent of the value of any asset they take as collateral.

Example #1:

Your business applies for capital. The lender wants collateral as security and tells you real estate is required. Because you need a large business loan, you agree and pledge residential real estate.

Your home is worth $300,000. The lender has a maximum LTV policy of 75% against real estate.

In this example, the maximum amount would be $300,000 X .75%

= $225,000. If your home is free and clear and the lender agrees to a 75% LTV, then expect $225,000.

Example # 2

Instead of real estate, you put up equipment or vehicles. The amount offered will be much lower. 35% to 60% is the most common range, depending on the lender and only based on the equipment they choose to accept. Lenders rarely are interested in all of the equipment available but may take a blanket lien anyway.

You provided an equipment list with $100,000 in equipment. The maximum Loan to value, LTV is $30% but you are only getting $15,000. What happened? The lender likely only is interested in $50,000 of the $100,000 in equipment. As a result $50,000 X .30% = $15,000.

2. Use valued assets to boost your Approval amount.

Example # 1:

A business loan applicant qualifies for $25,000 in business bank statement loans, but they really need $75,000. The borrower pledges their vehicles and construction equipment to try to get more.

The retail value on the equipment is $150,000 and the lender comes back with a 40% LTV. This equals $60,000 combined with the $25,000 the unsecured option. Combining the two, the lender is agreeing to a maximum of $85,000. By using the 40% loan to value against the equipment, the borrower is able to boost the offer by $60,000.

Knowing this, applicants can estimate what lenders will do in advance for the collateral they have. The borrower can use that information to decide if they should apply for an unsecured line, or secured with assets.

3. Negotiate

Almost all borrowers think they cannot negotiate and do not have any power when it comes to the borrowing process. The borrower does not have the upper hand, but they can get a lot by taking the right steps at the right time.

Negotiate during the request. Even if they decline what you are negotiating for, you may still get other improved terms if you had only asked for them.

Ask for higher amounts, longer terms, better rates and early payoff terms. The lenders is not going to give you better terms unless you ask for them.

First decide if it is worth it to use your assets to get money?

If you must have more money, then you must use your assets. Strong cash flow and credit are the best ways to get an unsecured business or personal loan instead.

The borrower has to decide if the risk they go past due is high and whether they can afford to lose the collateral. The risk is high when the borrower cannot run the business without the equipment.

5. How to get the highest % Loan against the value of assets.

Listed stocks, certificate of deposits and any other liquid security usually brings the highest loan amount. This can be up to 100% because while the balance owed goes down, the value of this collateral does not. Listed stocks is an exception that can decrease in value.

Real Estate also brings a high loan amount as a percent of it’s market value. Most real estate backed transactions are in the 65% to 85% of the market value.

After real estate, percentages drop down a lot. Equipment usually brings between 35% and 50%. Traditional banks rarely makes these types of deals and usually only offer 10% to 15%.

6. How credit affects LTV Loan to value

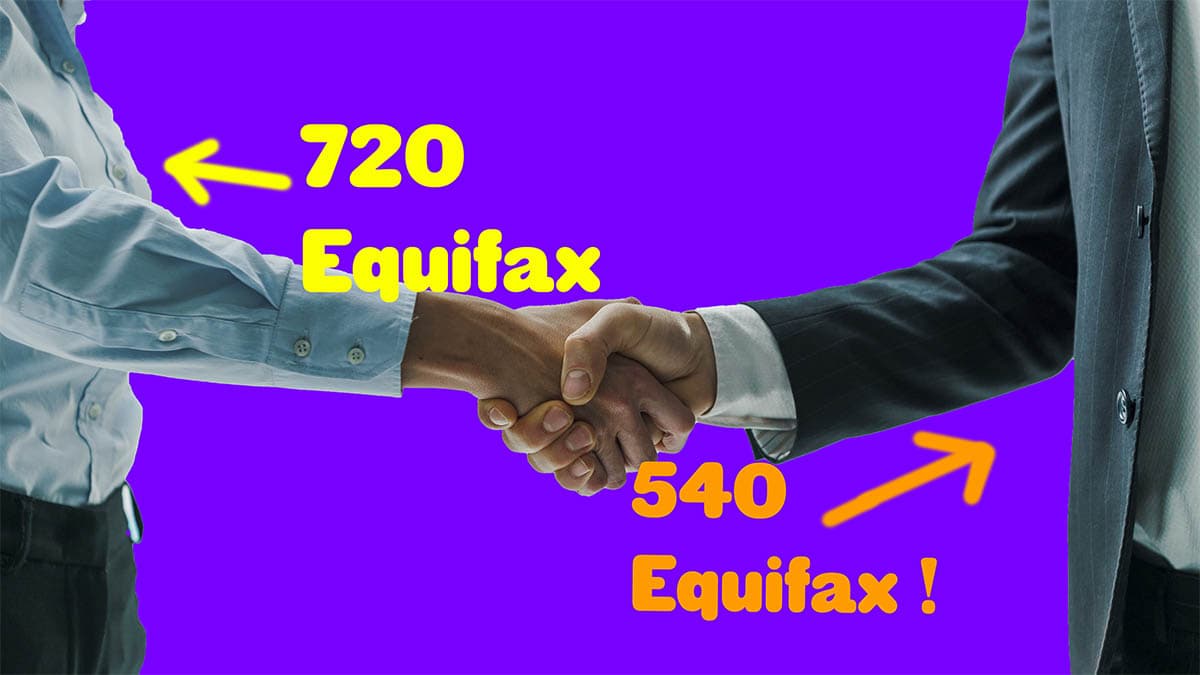

Credit scores have a strong impact. The same applicant with a 700 credit score may get a higher approval than a 575 credit score with the exact same profile.

Lenders will approve more on secured transactions for borrowers with a higher credit score. Lower credit scores are always considered a higher risk and the numbers go down.

Example:

An applicant with a 725 bureau score uses their free and clear commercial property to get financing. The property is worth $1,000,000. They go to a bank that approves a maximum 75% loan to value against real estate.

This applicant that has a 725 credit score gets funding with a 75% LTV, which equals $750,000.

An applicant with a 600 credit score gets a 60% LTV maximum, which equals $600,000. This is common in practice. In this case, an applicant can get $125,000 more or less, depending on their credit score.

7. Valuations: How appraisals fit in

Many asset based loan offers use valuation tables and market estimates to arrive at the amount.

Provide any recent appraisals you have that are less than 6 months old. Doing so should protect you from getting low balled.

Consider ordering an appraisal when you get an approval you think is too far below market value. Lenders tend to make conservative estimates that help them, not you.

FAQ on Loan to Value.

What is Loan to Value?

The amount a lender will offer as a percentage of the market value of assets. Collateral valued at $100,000 with a 60% loan to value may result in an offer of up to $60,000.

How can loan to value help me?

It helps borrowers decide whether to apply for secured or unsecured financing. It also helps them understand what types of collateral give the lender. The biggest benefit is that is brings larger approvals.

What can I do to get a higher offer?

Call the lender and ask what types of collateral they will accept and what percentage they will loan against it. Real Estate will bring the highest amounts.

Why is the lender approving such a low amount compared to the value of my asset?

It is usually because they only offer a maximum percent of the value depending on the type. They want to get their money in case of a default by approving far less than the market value.

Conclusion

Negotiating after you have been approved may get you some concessions in terms from the lender. Ask for a higher amount when you know the offer is too low compared to the market value.

Understanding what loan to value is and how to use it can help you get approvals for higher amounts and terms more favorable to you!

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.