Not enough deposits: Merchant Cash Advance Declined.

Your business has been declined for a Merchant Cash Advance or ACH bank loan. There are several things that your business can do to get an MCA merchant cash advance. It may

have to take some time to correct or change things that caused the decline.

Many business have one or more MCA Merchant Cash Advances and ACH loans to finance their businesses. There are many reasons businesses are declined for these merchant cash advances when they apply. The dollar amount of the monthly deposits, the number of monthly deposits and NSF and overdrafts may be too high. Click on one of the links below to try to get approved for a Merchant Cash Advance.

Data Secure 15 Second Application Here!. Add Email and name to access App. Attach the last 3 months bank statements, or send App only.

Or tap TEXT US, and Text contact info.

To Call tap Tel # link, CALL US, Press Dial.

We can work with businesses to get past decline reasons, get approved and get financing.

List of the Top 9 Reasons why your MCA was declined

Top 9 Reasons Your MCA was Declined:

1. Affordability

This MCA decline reason means your company cannot handle the new payment without significant problems. This is often a decline

reason when your total monthly deposits are under $10,000 per month.

If you know you can manage the payment, then prove it! Provide your current bank statement, other accounts you may have, or tax return that shows you have the cash flow.

Make sure the investor isn’t using the lowest month to make their decision. Ask them to use the average of your deposit totals for your most recent 3 months.

This almost always happens when the business has cash flow problems during the current month.

The verification failed for either low deposit volume, overdrafts and NSF’s, or not enough individual deposits. It is usually some combination of these issues.

Ask specifically what they saw in the current Month that they don’t like.

Decide if this can improve enough to qualify in the next few days. If not, apply above to get another funding option.

4. Credit Score Too Low:

Some programs require a minimum credit score of 550, 600, or even 650.

Find out what score is required. If it is too high, apply for a program that will accept your credit score before you apply.

Ask the lender what minimum sales amounts are they looking for?

Also ask how much do you need to put into your account in the next week or two to qualify. By doing so, you may be able to qualify before the current month is over and not have to wait until the next month.

6. Recent Overdrafts or NSF’s:

Overdrafts or NSF’s in your checking account in the last 3 months were excessive, and why your MCA was declined.

Add up exactly how many Overdrafts and NSF’s you had. Ask the lender what the maximum is and how long before you will qualify.

7. Not Enough Deposits Per Month:

There were not enough individual deposits. Some funders require 5 or more each month.

Make more frequent smaller credits if possible.

Find a source that will accept the number per month you are now making until you can start making more. Ask in advance what their mimimum is.

8. Time in Business Too Short:

The time in business is not long enough through the Secretary of State or on your License.

Ask the funder how long they require. If you are within 30 days of the minimum, then ask for an exception.

If they refuse, then find a program that will accept how long you have been operating.

9. Background Check Failed:

A background check revealed something they didn’t like. When you get this MCA decline reason, learn more about a Business Loan with a background problem here.

Ask the MCA company specifically what the problem was, and if that matches what you know to be true.

Shop other MCA companies that have programs that accept your background issue before applying.

Unsecured financing has less risk. You do not need to offer collateral with a loan against your assets.

Up to 18 Month Term options for 600 and 1 Year in business and higher.

Get money against your cash flow again after payoff. Use it to get money more than once.

Programs for as low as $2,000.

Lower offers makes this a better option than regular title loans. No need to risk your vehicle or equipment for a small amount of money.

Need more general info on developing your business? Visit the SBA for resources

such as local assistance, business guides and business plans.

Conclusion: Why your MCA was Declined.

Your MCA was declined for one of these reasons listed above.

Take the actions listed and you can still get an approval offer and funding quickly!

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

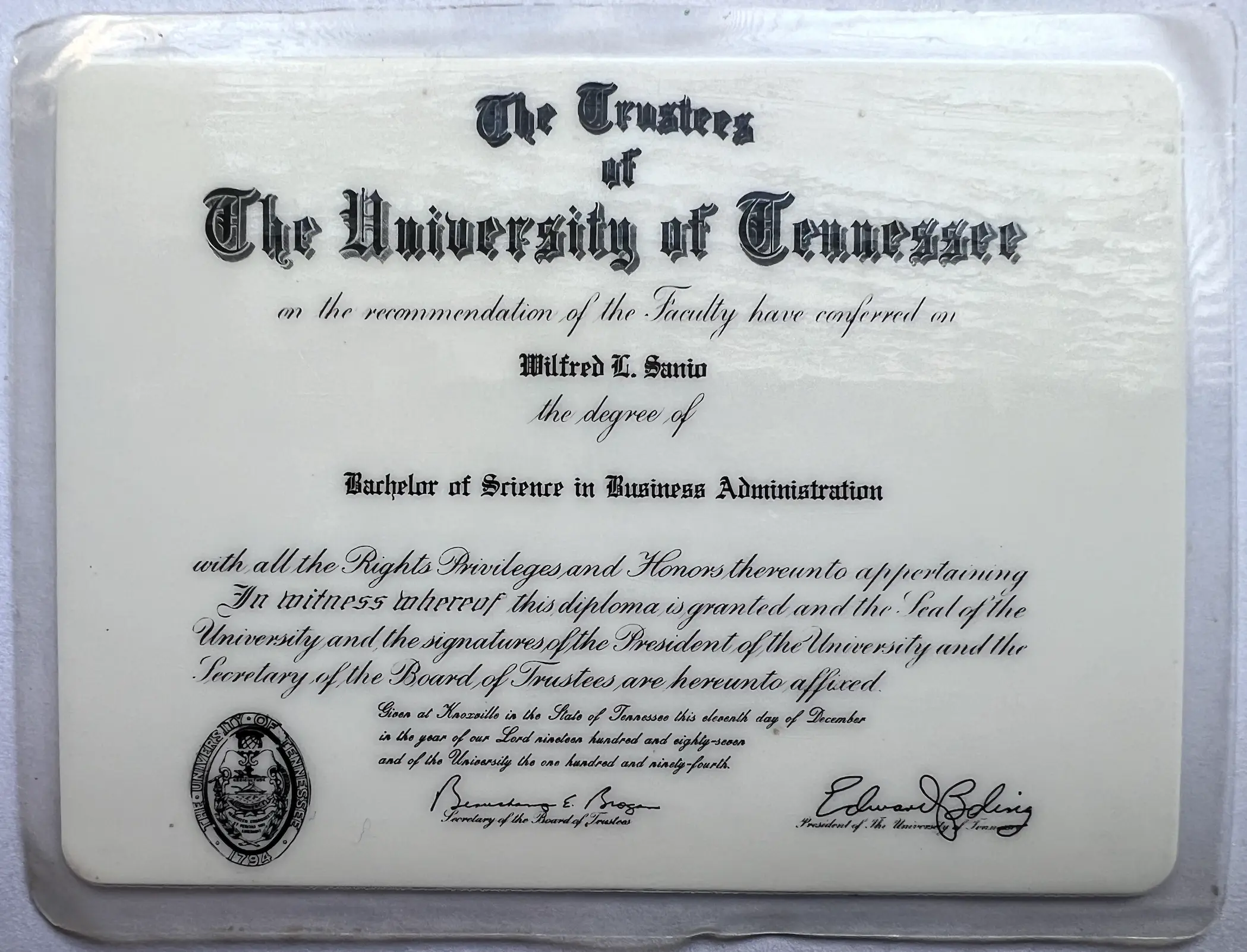

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Has your business has been declined for missed mca payments? You don’t need to settle for a denial anymore. There are other creative options to get approved and funding, today!

How to get a business loan with missed MCA payments:

Steps and tips on how to get a business loan after missing mca payments.

Tools needed: internet connection, computer, phone. Supplies needed: Time available

Step 1 Evaluate your missed payments.

The number missed is important. Missing 1, 2 or 3 payments is considered minor and should not prevent your business from being approved for more unsecured type bank statement loan funding.

Missing more than 3 consecutive daily advance payments may trigger denials with other lenders. Bringing your account current is the first step to get new funding.

Communicate with the lender during the process. Regardless of the outcome, it almost always causes the lender not to take more adverse action against you when behind. It will also make new funding much easier.

Evaluate your missed payment status

Step 2 Match funding options

Tip: Begin a search for other funding options. Start the search broadly with other programs that your business may qualify for. Decide which programs are the best fit for your business.

Look at the qualifying requirements for other programs. Eliminate those programs that your business likely could not qualify for. Prioritize and choose programs you can get approved for instead of programs you prefer.

Match the best programs that best fit to your business.

Step 3 Apply

Apply for the best matching program that allows for recent missed payments on other financing. Talk to a representative before applying when possible.

Tip: Give them information on your overall profile and discuss your chances. If it is still a good fit, then apply.

Step 4 Close approval

Review terms and conditions of any approval offer. Close the transaction if your business can handle the payments and the funding will assist in generating future revenue.

Step 5 Make a plan after denial.

If the request remains a denial, then make a plan. Understand the decline reasons. There may still be a chance to reverse the decision and get an approval. Try this first. Consider applying with other lenders when you cannot get approved.

Apply with other lenders. If that still does not work, do not stop the process.

Begin working on correcting the reasons that were used for denial during the first funding request. Whether it is credit, financials, or cash flow, try to improve this month over month until your profile meets the requirements of the previous lenders.

Make a short term plan if the denial remains in place.

FAQ: How to get a business loan with missed mca payments:

Can I get a business loan with missed mca payments?

Yes, you can get a business loan with missed mca payments. Review the decline reasons with the lender to see if the decline can be reversed. Finally, you can work on correcting the denial reasons to get funding.

Can I get another cash advance after missing payments?

It is possible to get another approval. An offer will depend in part on how many were not made, when they happened, and if they are still past due. Getting the account current is the most important step. Staying in frequent communication with the lender will help your chances as well.

Do missed cash advance payments show on my credit?

Untimely payments do not show up on your personal credit report if the lender has not declared a default. Default accounts may show up on personal or business credit. Check your contract. It may provide information on how and when the lender reports delinquencies.

Conclusion

Being declined for missed mca payments is something that can be overcome. Don’t wait several months to get funding.

Try to reverse the decline decision with any current lender. Look for lenders that will approve your profile the way it is now. Then work on correcting all your main decline reasons for the future.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Are Recent Low Sales keeping your business from getting a loan?

For many businesses, low sales months cause business loan declines, especially when deposits are under $10,000 a month.

Read the full Article here: Deposits under $10,000 a month.

FAQ Frequently asked questions on getting a business loan with low recent sales

What are slow sales considered?

When sales are less than normal for a specific time period. Lenders consider any reduction of sales of more than 25% to be a significant reduction.

How do lenders look at a major decline in sales?

Lenders want to know why were sales low and for how long. They also want to know when sales are expected to rise again and how much. Lenders also look at the percentage drop in sales. If the business can survive, pay all expenses and make a profit are then evaluated in the loan decision.

How can I get a business loan when we are operating at 50% capacity?

There are several other types of financing a business may still be able to get now even with a big drop in sales. Asset based financing is the most likely, including using receivables, equipment or real estate.

My business tax returns last year were good. Why did the lender still decline us for the recent drop in business sales?

The lender is looking closest at the condition of your business right now and in the future. Lenders see a recent big downturn without knowing when sales will go back to normal as very high risk.

Have your business sales been low in the last few months?

Many businesses have had low sales during part of the year and as a result, have trouble getting financing.

Save your time. Don’t spend weeks racking up hours and inquires applying with lenders and programs that are almost certain to decline your business. Apply with programs that will lend even with much less demand during the virus. Get funded now. Apply above.

Can we get business funding with no recent sales?

What are examples of declines in demand?:

December, January and February were much slower sales due to seasonal business.

The most recent (3) months sales are looked at. The total deposits per month are reviewed to determine trends. Questions by the lenders include:

Is there a downturn? If so, how much? What were the customer’s average daily balances? Were they overdrawn with NSF’s and overdrafts?

50% or 60% reduction in sales

Lenders look at how much of a reduction in business your business has had. How steep of a reduction, how quickly, how long and has the business started to recover? The main thing lenders will look at is the percentage sales drop. Any drop in sales over 25% is considered significant. Funding may still be possible with drops of 50% to 75%. If a business has had a major drop in month to date revenues but still needs a larger business loan, then they can add real estate to back the funding and get a much higher loan loan.

Some segments of your business were strong while others had very low sales.

Example: A retail store’s overall sales in March, April & May were down 50%. In store customers dropped to almost 0 because of the lockdown. However, because their website offers shipping and delivery of products, online sales were up 75%.

How to get a small business loan in spite low recent sales?

– Make your case. Don’t just say business was bad. Say more. Example: Explain why. You can say “We had a drop in business and purchases because of the virus. In spite of that, we are now open and sales are increasing”.

Tips and steps to explaining low recent sales to lenders to help get a business loan

In the example above, provide the information when applying. Explain how it was not the fault of your business, and you still had sales that are now increasing, both positive current trends. This shows that your business overcame obstacles and is rebounding.

Have all the following questions already answered about the slowdown in business and provide them when you apply.

Why?

How bad has it been?

What is the situation now?

How has it affected your business?

What are you doing about it?

When do you expect sales in rebound and increase?

How can you show the business will survive?

If your business has started to recover in May, consider loan options now.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Has your business been declined for not having enough collateral?

Then choose from a small business loan that has 5 very flexible no collateral options. Click on the Info Form below because fast as same day funding is just a click away.

You may still able to negotiate. Lenders often want too much collateral and borrowers do not push back. Sometimes lenders won’t accept high value vehicles because they need repair. Use a truck repair loan to get broken down assets in operation again and qualify as acceptable collateral.

Business funding does not have to be hard to get. Does your business have collateral or cash flow? If so, there is a program that will fund your business. Requests for higher amounts are much more likely to be declined for the applicant not having enough collateral. Denied for not enough collateral? See Tips, FAQ questions and answers below.

The most flexible business loan collateral options of all programs. If it can be used as collateral for a business loan, it will be!

Frequently asked questions FAQ declined for a business loan for insufficient collateral.

What does insufficient collateral mean?

You or your business did not have the assets that lender wanted to approve a loan. We specialize in funding business loans against collateral large and small using many asset types and with the toughest credit a borrower can have.

What can be used as collateral for a secured loan?

We can use equipment, vehicles, semi-trucks, trailers, and real estate for hassle free and quick funding.

What if I don’t have collateral?

A cash flow or unsecured loan can be approved. Pre-qualify immediately and get an approval and funding within hours in many cases.

Why do some loan companies want collateral?

To approve a business loan instead of declining it. The lender can sell the collateral if a borrower defaults and recover what is owed to them. This lets them make more and higher offers.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Sales as little as 3 months Brand New Businesses

Asset based options and fast closing!

Low credit scores and large approvals available. Apply below

Options

declined for a business loan?

3 Month time since start date program

Your company can get money as fast as one day. Provide the most recent (3) months company checking account statements with the one page application above, and you can be on your way to funding within 1 or 2 days.

1 Month time in business Program.

Get a large business loan in you have been operating for more than 1 year. Many applicants get up to 75% of their total monthly deposits.

Low credit score program

Were you turned down for having a very low credit score? Apply for the low credit score approval program and turn a decline into an approval.

We will help you get approved for time in business.

FAQ Frequently asked questions.

What is time in business?

The time starts from the day the company is registered with the secretary of state, city, or county. It is not the time when revenue has started. Some lenders will look at when the company began having sales as part of their review. Can we get approved with a few months open?

Cash flow programs for as little as 3 months operating or less are available. Certain asset based programs can be approved with only 1 month. Can we get a loan being brand new?

There are multiple programs available if you just started. Even companies that have been registered for only a few weeks have an opportunity to be approved. Why do lenders decline new businesses?

Lenders have statistics that prove the longer companies have been open, the more likely they will stay open. Businesses operating more than 3 years are successful for a significantly longer time.

In summary

Our programs can get you approved today with only 3 months or less since your starting date. Just because you are new, we won’t stop you from capital.

What are non sufficient funds and overdrafts? A overdraft or insufficient funds is a negative balance in a bank account caused by drawing more money than the account holds in part because of low deposit volume.

How can your business overcome being declined for a business loan or Merchant Cash Advance for having excessive Overdrafts or excessive NSFs? Here are several tips that your business can follow to get a business loan.

You will get you the best program for your business. Don’t forget to be ready for the business checking account verification.Apply below today.

Business account overdrawn.

We assist businesses in overcoming these obstacles so they can focus on making their business prosper.

Many times a business loan that is approved falls through at the last minute and does not close if there are overdrafts and NSF’s before closing. If there are too many overdrafts and NSF’s since the beginning of the Month, or between the time of approval and closing, it may be declined just before closing. When a Bank verification is done and the Account is overdrawn, the loan may then not close and be declined.

At the time you are trying to close a loan with an overdrawn business account, make a deposit immediately before the Lender checks the bank account. If you make a deposit beforehand, you can save the approval. If it is too late and the loan is declined, ask the Lender if you can make a deposit to bring the account into the positive will they close the Loan then? Do not try to close a loan if your account is overdrawn. Wait until it is in the positive.

FAQ Too many overdrafts and nsfs

Can we get a business loan with nsfs and overdrafts?

Approvals are issued everyday to businesses with nsfs and overdrafts in their checking account. Having enough cash flow to pay the debt and only having overdrafts occasionally helps. Provide a good explanation for why the account was overdrawn when applying.

How hard will overdrafts and nfs make it to get a business loan?

Overdrafts and nfs do not always keep your business from getting approved. You may get approved for a lower amount with higher rates and shorter terms. Overdrafts in your business checking account in the last 30 days are more important, and the last 90 days are usually looked at. Rules on the maximum vary from lender to lender.

How many overdrafts and nsfs can we have?

Most business loans limit overdrafts and insufficient fund items to about 5 per month. Ask specifically for any business financing you may apply for. Some programs will not allow more than 3 recent overdrafts in the last 30 days.

Why were we declined for paid nsfs?

The lender probably declined because they felt the cash flow and average balances were not strong enough. Even when insufficient fund items are paid, they still happened and the lender may believe any new debt will be too much.

How to get approved with excessive Overdrafts or NSF’s

Talk to lenders in advance and find out if the lender has a maximum number of Overdrafts or NSF’s per month they accept. We can put your business into qualifying programs so your business can get all the Capital it needs.

Business Loans with Overdrafts and NSF’s

Other options if declined

Too many Overdrafts or NSF’s for an MCA merchant cash advance or ACH bank loan.

Talk to the Merchant Cash Advance companies and ACH business loan lenders directly about being declined for having too many Overdrafts or NSF’s per month. Ask them if there are other programs available you may qualify for right now. Always ask if you can start out for a lower amount.

In addition, make sure your business does not have any more Overdrafts or NSF’s for a few weeks and apply at the start of the next statement month.

Possible solution:

If you know you will not have any more Overdrafts or NSF’s the next few weeks in your business checking account, tell the Merchant Cash Advance company or ACH business loan company. If the overdrafts or NSF’s were from a single event instead of spread out throughout the months, this can make a difference. It is an isolated incident. Let the lender know they resulted from a one time event. Many decisions are automated and made quickly. Make a strong case and the lender may reconsider your request.

If the lender will still not approve it, ask how long you have to wait before your can be reconsidered. Ask what needs to be corrected to avoid being declined again.

Get other working capital loans

Your business can apply for other types of business loans if time is critical. Which ones are best depend on your company’s financing needs and situation. Choices include:

Also consider business loans based on Real Estate, Equipment Assets

that are free and clear, and Account Receivables. Monthly Term loans up to 60 months or longer with full financials.

Your business can overcome being declined for a MCA Merchant Cash Advance or ACH business loan for having too many Overdrafts and NSF’s. The SBA small business administration offers advice and workshops on business loans.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Has your business been declined for a loan for not making enough deposits into your checking account every month, or having under $10,000 a month in deposits?

Get approved and choose one of severalsmall business loans for your business that do not require a lot of deposits per month. Apply below and get approved today.

Contact us and we will put your business into the approval program that can accept less than 5 deposits per month. Only have 1 or 2 deposits per month? We have programs waiting for your business now that can you approved fast. Contact us above!

FAQ on being declined for a business loan for not having enough deposits

How many deposits does our business have to make each month to qualify?

5 deposits or more per month are usually required for a merchant cash advance. Some advance companies require as many as 10 or more. They must be real business revenue from customer sales and not transfers between accounts.

Can our business qualify with only 2 or 3 deposits per month?

Some lenders consider a low number of credits per month into a business account as higher risk because the business has fewer customers that it makes money from. Losing one customer will cut revenues and their ability to repay a loan much more than a business with many customers.

Why were we declined for not enough business deposits when we had more than 5 per month?

Deposits that are not from the sales of the business may not have qualified as revenue. Examples are transfers from other accounts, loan proceeds, very small deposits compared to others, and rebates.

Businesses have used cash flow loans to a great extent in recent years to finance their businesses. The business account has low recent sales in one of the most recent months.

Make more deposits immediately during the rest of the month and apply at the start of the next month. A deposit to a business checking account statement is often from several customers. Retailers usually have several checks and cash from several customers, go to the bank and make 1 deposit. Instead of 1 large deposit, break the deposit into several smaller deposits over the course of 2 or 3 days.

Talk to the Merchant Cash Advance companies and ACH business loan lenders directly about being declined and ask them how you can get your business approved. As your business grows, it will add more customers. Having deposits from more customers will increase the number of deposits per month into your business account. As a result, this will make your business a better risk from the lender’s point of view. The number of customers a business has is an important part of looking at risk by lenders.

For example, restaurants have hundreds of customers per week. As a result, they will show many deposits per month. Restaurants that lose a few customers only lose a small percent of their customer base. A business that has 4 large customers loses 25% of their customer base when they lose just 1 of their customers.

Possible solution:

If you know the deposits you make into your business checking account have multiple items, you can tell the Merchant Cash Advance company or ACH business loan company.

What are multiple items?

Multiple items means that the funds in the deposit are from more than 1 customer. If the merchant cash advance company knows this, you can get a copy of the deposit from the bank. The copy of the deposit will show the items deposited. If it is 5 items, you may get credit for 5 deposits instead of 1. You may be able to get the MCA company to change the decline to an approval. A number of ACH lenders and merchant cash advance companies are open to this.

If this does not work, ask how long you have to wait before they will consider you again. Be clear on what they want to see the next time so you will not be declined again.

Get working capital through other loans

If the options above do not work or you cannot wait, your business can consider other types of business loans. Which ones are best depend mostly on your company’s profile. Choices include:

– Monthly Term loans up to 48 months based on Tax Returns

– Accounts Receivables Financing

– Business loans based based on Real Estate or Equipment Assets.

Business loans based on real estate, equipment or accounts receivables will usually not have this requirement. Having collateral that covers the loan amount means that cash flow is not as critical. The number of customers is also not important.

Unsecured loans depend heavily on cash flow and as a result, the cash flow of the business is scrutinized much more. Businesses applying for unsecured loans should also have financial statements that show the business making money and having net income. Many businesses do not show net income and this hurts their request and also causes declines.

The SBA small business administration also has excellent resources on alternative business loans

Video Description:How to get a business loan when lenders consider your industry to be restricted or prohibited. In summary, they don’t like what your business does. Examples of affected business types and options.

Restricted Industry Business Loan (Video Transcript: Click to Expand)

Introduction

[ city street sounds ] Welcome to smallbusinessloansdepot. [ young woman says Ooh! ]

Loan Options for Restricted Industries

Do you have a Construction company or other practices that are being denied by traditional lenders for restricted industry? Click on the link below, smallbusinessloansdepot.com. We have loans available for flexible and restricted industries that most lenders do not want to work with you because they send you a letter that says you are considered a restricted industry to them. We have programs specifically designed for many industries that have difficulty with traditional lenders.

How to Apply

Click on smallbusinessloansdepot.com.

Call to Action

Complete the contact us form today. Get started today on financing. Don’t spend your time having lenders tell you that they think you are a restricted industry. Call us today for financing. Call us at 919-771-4177 or go to smallbusinessloansdepot.com. On you tube, please subscribe, like and share.

It is when your operation type is considered risky and undesirable by lenders such as a loans for used car dealers. Other companies such as adult or porn, attorneys, financial services such as check cashing are restricted from doing business with you, and investors do not even want to lend to you. Author Biography: Will Sanio

Fast and easy programs. The highest approvals with best terms available, including new programs in trucking such as a truck repair loan to fix your vehicles. Also find out if you might be considered a HIGH RISK ?

Let others say no. We say YES! Apply Below now & get a loan today!

Use the lists provided below to determine if your type may be considered restricted by others.

Identify investors and sources that will loan to your sector. Contact them and ask for their qualifying criteria. Select the best match based on your needs and their approval criteria.

If approved, request and review closing stipulations and documents. Submit all required closing documentation. Complete merchant call if required.

Receive funds into your checking account.

Find a loan product here regardless of industry type.

Restricted industries or elevated scrutiny businesses – Types:

“Restricted Industry List”

Accountants, Accounting firms, Accounts Receivables Factoring.

Adult Entertainment, Escort Services, Gentleman's Club, and adult industries.

National and Regional Airlines.

Attorneys

ATV Dealers, ATV Sellers and RV Dealers.

Auto and Home Supply Stores.

New Auto Dealerships and used car lots and dealerships.

Auction Houses.

Bitcoin.

Bus Companies.

Construction.

Cemeteries and Funeral Homes.

Consignment Stores, Child Day Care, and Churches.

Collection Agencies, Check Cashing, and Bail Bonds.

Credit Reporting, Protection and Restoration.

Consulting.

Collection Agencies, currency exchanges, and Wire Transfer.

Criminal conviction, arrests by owner. This may include past

misdemeanors or a felony offense.

Dating and Escort Services.

Debt Consolidation.

More Examples:

Direct Mail.

E-businesses and Commerce.

Educational, Colleges and Schools.

Factoring, Financial Institutions, Financial Transactions Firearms sales, weapon sales

Financial services and lending

Financial Transaction Processing, Financial Advisors and Freight Forwarding Forwarders.

Fitness and Recreational Facilities.

Fraternities and Sororities.

Freight Brokers.

Gambling and Gaming Establishments.

Gas Stations.

Holding Companies, Insurance Agencies, and Investments.

Home Building, construction, and housing related.

Home based.

Horoscope and Fortune Telling.

Import and Export.

Income tax return and preparation.

Insurance Agents and insurance brokers.

Internet and online

Insurance Agencies, and Investment Opportunities.

Lawyers.

Lotteries and raffles

Further Examples:

Kiosks. Lawyer and lawyers. Attorney and Attorneys. Legal practice and Legal Practices. Marinas. Mining and Quarrying. Magazine Subscriptions, Mail Order Coin Sales, Mobile Home Dealers, Mobile Phone Dealers, Wireless Stores and Cellular Stores. Mortgage Lenders and Mortgage Reduction. Motorcycle, Scooter, Motor Home and Camper Dealerships. Night Clubs. Non Profit and Grant Writers. Non Bank Cash Advance. Oil Pipelines and Gas fields. Online Stores, Online Retail Stores, Online Merchants, and Online sales. Payroll advance, Pawn Shops, Thrift Stores and Consignment Stores. Personal Trainers. Precious Metal Sales and Coin Sales. Printing and Printers. Real Estate Management, Investment, and Brokers. Recreational Vehicle Sales.

Restricted types continued:

Schools.

Sports Events Advice, Sports Instruction and Recreation Instruction.

State Agencies and Government Agencies.

Taxi and limousine service.

Ticket Brokers, Time Share Investments and Tour Guides.

Travel Agencies and discount clubs.

Tobacco and Electronic Cigarettes, Firearms and Gun Stores.

Trucking, Transportation, Logistics, and Sea Transportation.

Used Car dealers, Auto Dealers, new car dealers and Truck Dealers.

Used Furniture Stores and Furniture Retailers.

Vehicle Inspection.

Virtual Auction Houses.

Vitamin Retailers.

Wholesale Clothing.

Wireless phone and accessories.

Elevated Scrutiny Industries

Other sectors are included in "elevated scrutiny".

Home health care.

Web development, Credit and debt counseling. Financial advisors and consultants.

Elevated Scrutiny often includes:

Annual Membership Clubs.

Appraisal Services.

Auction Houses.

Benefit Packages.

Boat Sales.

Buyers Club and Coupon Books.

Detective and Private Investigation.

Donation. Door to Door Sales.

Employment Agencies.

More elevated scrutiny industries:

Financial Aid Services.

Flooring, Tile, Blinds and Windows.

Formal wear.

Fortune Tellers, Psychics, Astrologers and Spiritual advisors.

Furniture Stores, Homeopathic Remedies and drugs insurance.

Modeling Agencies and Beauty Pageant Organizations.

Mortgage Lender or Mortgage lenders

Multilevel Marketing and Pyramid Sales.

Online Electronic, High Ticket Electronics, Prepaid Phone Card and seminars.

Sports Memorabilia.

Telemarketing, Ticket Agencies, Time Share.

Web Design and Hosting.

Utilities.

Seasonal and challenged industries

Challenged industries are similar to those that get elevated scrutiny. Underwriting will consider them, but under a tougher approval process because of what they do.

Construction Companies:

Lenders often have many restrictions and high scrutiny for construction. They are either automatically declined or are offered lower amounts with shorter terms.

Insurance Companies and others:

Insurance is hard to get funding for. Insurance companies receive commissions for policies sold but then the have to pay the insurance broker who sold that policy.

Another example is a travel agency which also keeps a small percentage of what they receive and pays out the rest.

Convenience stores that sell gasoline often have to immediately pay back out a high percent of those sales. As a result, most of the revenue they show coming into their account goes right back out.

Lenders have to make a decision and approval amounts based on their net income.

Seasonal Companies

What is a Seasonal Business?

Any company that has peak sales and operations during the same months every year. The rest of the year they are either slow or closed.

They are especially scrutinized by lenders who will ask for more documentation such as additional years tax returns and payback months bank statements from previous years.

Examples of Seasonal include:

Accountants and Tax Preparation Services.

Bridal Wear, Catering Halls and Floral.

Moving and relocation.

Jewelry, Shipping, Golf Courses and Ski Resorts. Other seasonal operations are nurseries, ice cream shops and amusement parks.

Example: Customer Case

Santa Fe, NM. Pueblorides, a used car dealer completed a $45,000 working capital line. They are a small used car dealer in the Pueblo, NM area. Used Car sales are almost always a restricted industry and we are able to assist them. They were turned down by several banks. With this funding, they were able to increase the number of vehicles on their lot.

Getting funding in a restricted category

Businesses that have been denied for the type of operations they have must find a reliable partner. Ask upfront if they work with you and consider a loan.

If the investor has categories like this, they usually don’t want to tell you. Ask what type of loans they like to do. These questions will point you in the right direction and avoid unnecessary declines!

FAQ Frequently asked questions.

How do I know if my business is considered restricted by lenders or not?

Ask before applying if they have programs available for your type of operation, because sometimes they don’t want to tell you. Our loan programs lend to all sectors.

What does restricted industry mean?

A business whose type of operation has much stricter rules for approval. Other lenders stay out of it because they see it as a higher risk for delinquency, defaults and losses. Sometimes they just don’t have expertise in that field.

What do challenged and prohibited industries mean?

These are industries lenders will scrutinize much more and require a longer time in business, higher credit scores and revenues. Used car lots, construction, and trucking are examples. Ask if they have any limitations on lending based on your type of business.

Are new companies restricted by lenders?

Many loan companies do not loan to start ups. Check before applying if start ups have restrictions or are prohibited. Our programs work with 3 months in operation and longer.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank headquartered in Winston-Salem, North Carolina, and First Atlanta Bank in Atlanta, GA. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Are you asking yourself why the bank declined my business loan?

Where can you be approved? Helpful tips to turn a decline into an approval and find other business loans. Match your business to small business loans that you will get approved for !

What caused my business to be declined and what are the most common decline reasons Common reasons are:

If you have been turned down for any decline reason, contact us. We specialize in difficult to approve businesses and business loans and have programs that can approve your business for any decline reason.

If you think the bank declined my business loan for wrong reasons, then the first step is to call up the company that turned you down.

Determine if you are speaking with someone that has the knowledge and experience to provide you with useful information about the decline. If you received a letter, call and confirm the decline reasons.

For more information on strategic reasons, read why banks don’t lend to small business.

Reasons why your business loan was declined

FAQ Frequently asked questions on why the bank declined my business loan

Why don’t banks lend to small businesses?

A high percent of small businesses fail in the first 5 years, so they are considered a higher risk than larger businesses. A small business has to have excellent personal and business credit, strong collateral and financial statements to get approved at a bank. In most cases only certain collateral is accepted that can be easily liquidated with a value between 200% and 1000% of the amount of the loan. Financial statements must show steady or increasing gross profit and net income.

Are there alternatives to banks for business loans?

You can successfully get a business loan by understanding the different alternatives available in the marketplace. Then understand what it takes to get approved and the reasons you may be declined. Understand the strengths and weaknesses of your business and apply for the best matching program.

What can I do after the bank declines my business loan?

Ask a loan officer to discuss all of the decline reasons. Also ask how you can correct those to get an approval and if there were any other concerns. Get information as specific as possible and consider alternative business loans while you are working on the bank’s decline reasons.

More info on why the bank declined your business loan

Missed daily payments

You have an existing daily or weekly Merchant Cash Advance and you have missed payments on the advance. Missing daily payments is a major reason why a new loan request may be denied. Missed daily loan payments may can a renewal request to be denied.

Average Daily Balances too low

This decline reason means that your daily ending balances were too low over the month. Lenders have different balances that they want

and often will not tell you. Many lenders often want at least $1,000 Average Daily Balance consistently in your account.

Inconsistent Cash Flow

Business cash flow has fluctuated too much from month to month. In some months the cash flow meets the minimum required by the program and in other months it does not.

Declining Cash Flow

Total monthly deposits into the account have been declining month to month from recent low sales. Even if the average still meets criteria, the lender may still feel this is a reason for the turndown.

Does not meet criteria

This is a general decline reason. the lender does not want to tell you what this means

Month to Date MTD

This a decline reason that often happens with Merchant Cash Advances. The Month to Date activity is requested for the current month and the approval be declined or reduced when current months deposits are lower than the previous three months.

Ask if significantly lowering the amount of the request, adding a strong co-signer, or adding more collateral would cause them to reconsider and possibly approve the application. Speak directly with the credit department that makes the credit decision.

If any of the reasons you are declined for a business loan involve credit, you will want to contact at least one of the credit reporting agencies to determine what is on your credit file. You may already know most of what is on your file, though you should get a copy of your file to confirm it.

If there are any inaccuracies, you should dispute them with the bureau. This is easy to do and can improve your bureau without significant effort. You will succeed in getting derogatory information removed when the bureaus cannot prove the derogatory reporting is accurate.

Once you accept what is on your credit report, begin looking for other alternative loan options. First determine what are the strengths of your business and weaknesses of your business. When you contact companies, find out as much as you can about what their alternative loan options are based on.

Instead of choosing the business loans you like best, organize the loan types in terms of what your business is most likely to qualify for. Of those loan options, then decide which ones you believe you should proceed on.

Other Loan Options

Discuss the loan options with the representative and speak with someone who is knowledgeable, rather than someone reading from a script. If they don’t give you logical answers to your thoughts or concerns, try to speak with someone else. Don’t feel that you must get all the funds you need through 1 type of loan, or all of it immediately at that time. There may be 2 loan types that you should proceed on.

If your business needs $100,000 in total, and you only qualify for $50,000, this may still work by getting the funding in segments over time. You can take the $50,000 you qualified for and also work on getting the rest of the funding required over the course of the next few weeks or months. Chances are you did not need the entire $100,000 immediately. Most businesses that receive $100,000 do not spend it all within the first 30 days. These steps are important when your business has been declined.

For additional resources to help you prepare for future business loan requests, you can

also visit the SBA. The SBA government site has numerous resources which can assist your business.

Thank you for visiting our resource page on what to do if you are declined for a business loan.