Even more options are available on how to get mca merchant cash advances and accounts receivables financing. Merchant cash advance information includes getting low rate cash advances, the best renewal terms, and how to get out of a merchant cash advance if they are causing your small business cash flow problems. Excellent options are available for business owners with a felony or misdemeanor in their background.

Is your business having severe problems and is going out of business? Below are the Top 11 Reasons for going out of business followed by the complete list.

Take the fast, easy, and efficient steps to avoid going out of business. This may include securing working capital to bridge the difficult period. We have numerous options for all business situations.

Don’t let this happen to your business! Get funding today.

Top Reasons for going out of business

1. Running out of Money. Running out of money is probably the main reason for going out of business. There are different circumstances under which businesses run out of money. The business is going through a slow period. Revenues have been low since the business opened. Find out the top ways on how to get money to stay in business.

3. Too much debt and overhead. The owners or the business itself may have too much debt and overhead to deal with. They can’t handle it and go out of business.

4. Insufficient starting capital. Many businesses never really had enough capital to start. Often there are problems after opening. This is followed by the business not having enough capital to overcome them.

5. Unable to get financing or enough financing. Many businesses need working capital or other types of business financing after starting. Some of these needs are critical. If they cannot get the financing needed for equipment or short term working capital, the business may not survive.

6. Not enough back up capital or emergency capital. Business owners have liquid assets and net worth. If the business needs more working capital than

7. Bad Employees. This is usually employees that are bad performers with low quality work and low production. Some employees are out sick on leave a lot.

8. Bad Marketing and Sales. Some businesses have owners with expertise in certain areas. They may have technical but not sales and customer service. These other areas can be crucial to the survival of the business.

9. Inflexible ownership. This is resistance to change or new ideas. Many business owners have aggressive take charge personalities. This is often what drives them to accomplishing starting a business. It can hurt some business owners significantly. Many business owners are not open to new ideas or alternatives different than the ones they believe in. They are often very resistant to criticism.

10. Market changes. Businesses need to keep up with what is happening in their industry and stay up. Some businesses show poor awareness to market trends and changes.

11. Not keeping track of competition. Businesses that do not keep track of what the competition is doing may be left behind. Competitors may introduce new products, programs and incentives.

The reasons listed are usually the top reasons for going out of business. Some solutions and ideas are offered to avoid going out of business. If your business is closing, the SBA offers a list of items to consider when going out of business.

Not getting straightforward facts when applying for a business loan? Applicants are often told they are approved only to find out they are not. They are surprised they must pay significant fees at closing they were not told about upfront. Get money through credible, honest and upfront representatives.

Contact us and our reputable representatives will work with you as your business advocate, not a salesperson trying to sell you a product. Get full and thorough facts from representatives with integrity to put you on the path that is best for your company, not best for the lender.

You will be given a fair assessment of your chances for approval, the cost and charges. The strengths of your profile will be discussed, along with any weakness or obstacles to approval. You will be receive help with a partner that is looking out for your company.

Ethical business loan programs include:

– Money based on Gross Sales.

– Clear and plain english contracts

– Lines of Credit

– Asset based loans, such as loans against Tractor Trailers, Construction equipment

and Accounts Receivables.

– Financing to obtain equipment

– We specialize in difficult to approve customers due to credit, time in business, low revenues.

Free full consulting session.

Our consultants work much differently and discuss what is in the best interest of your company. We want to know what your situation is and what you are trying to accomplish. Basic facts are asked to determine all the realistic options. By doing this, you will only be talking about products that are the best match.

Then we will discuss their features and benefits. You can then decide which of the options are best for your business. You will not be pushed into any product. With this method, you can get financing in a legitimate and impartial manner. An authentic, true, reliable and objective assessment will be made.

You will get clear information upfront and what to expect. We build trust and trustworthiness by acting as your advocate. Get a transparent business loan.

For other broad loan options and assistance, check with the SBA.

Used Car Dealer Loans and used car dealer financing.

Loan for used car dealer up to $1,000,000.

Used car dealer loans of up to $1,000,000 can now be obtained fast. Terms available from 3 months to 120 months. Low credit scores under 500 and tax liens can be worked with. 3 Months or more in business.

What types of used car dealer loans can I get?

Used car dealers and new car dealerships now have fast business loan options. Programs are available. No financials or Tax returns are required.

Steps your used car dealership can take to get a used car dealer loan.

Search and identify lenders that have used car dealer loan programs and offer used car dealer loans.

For a used car dealership lot that has more than $10,000 per month in revenue and bank deposits, then it may pre-qualify for a business loan or other types of business financing. Short time in business less than 1 year can qualify.

Select the program that is the best match for your business and profile, such as revenue, time in business, and credit.

Select the program that is the best match for your used car dealership

Call the lender and ask for details on approval requirements.

If your business meets the requirements, then apply. Submit any information that will help your application.

If an offer is made for business financing, review the terms. If you want to close the transaction, gather all closing stipulations and close the transaction.

Buy here pay car dealers have always had difficulty securing business loans and rarely get financed by banks. Now they can use financing based on the cash flow of their dealership to get business loans fast. They need to make several deposits per month and keep at least $3,000 average daily balance in their business checking account.

New car dealer loans

New car dealers can also get financing using their revenues. The process is also fast and easy. Just a few business days for financing and a one page application.

Callers request a used car dealer loan, a loan for a used car dealer or a business loan for a car dealer.

Other requests include loans for a new car dealer, and loans for car dealers.

Callers this week have requested loans for a used car dealer and a business loan for a used car dealer. Other callers have requested used car dealer financing and financing for used car dealers. Our most recent customer specifically requested financing for a used car dealer. The most basic requests are car dealer loans and used car dealer loans.

Thank you for visiting our used car dealer resource page again soon.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

Start here for full LGBT small business loans and options. Equal access to business loans. Consider us for your gay business owner funding resources for alternative loans.

How are we different? We will first discuss your business in detail. Your future business goals and needs will then be reviewed. From that, the business loan products that are the best fit and can be approved will be discussed. We stay with you through the entire loan process.

500 and lower credit scores can be approved. Tax liens, short time in business accepted. $5,000 to $500,000. Short and long term loans. 3 months to 120 months. Fast turn around. Same day responses in most cases. Short 1 page application. Fast and easy process.

We will help you get an LGBT business loan fast through this program.

LGBT business owners sometimes encounter discrimination in the loan process. Our loans avoid these problems. There is full and equal access to business loans for the lgbt community. We discuss the specific needs of each business owner in detail. We help them determine the product that best fits their business now.

We work with and volunteer extra professional assistance to the community. There are many requests. Callers call in asking for gay friendly business loans.

Business Loan for Gay and LGBT businesses questions:

Are some of these lgbt friendly business loans programs specifically for the LGBT Community? No. These loan programs have been reviewed to insure they are friendly to the Gay and LGBT business community. All customers are welcome as well.

Business loans for Gay and LGBT Businesses Resources:

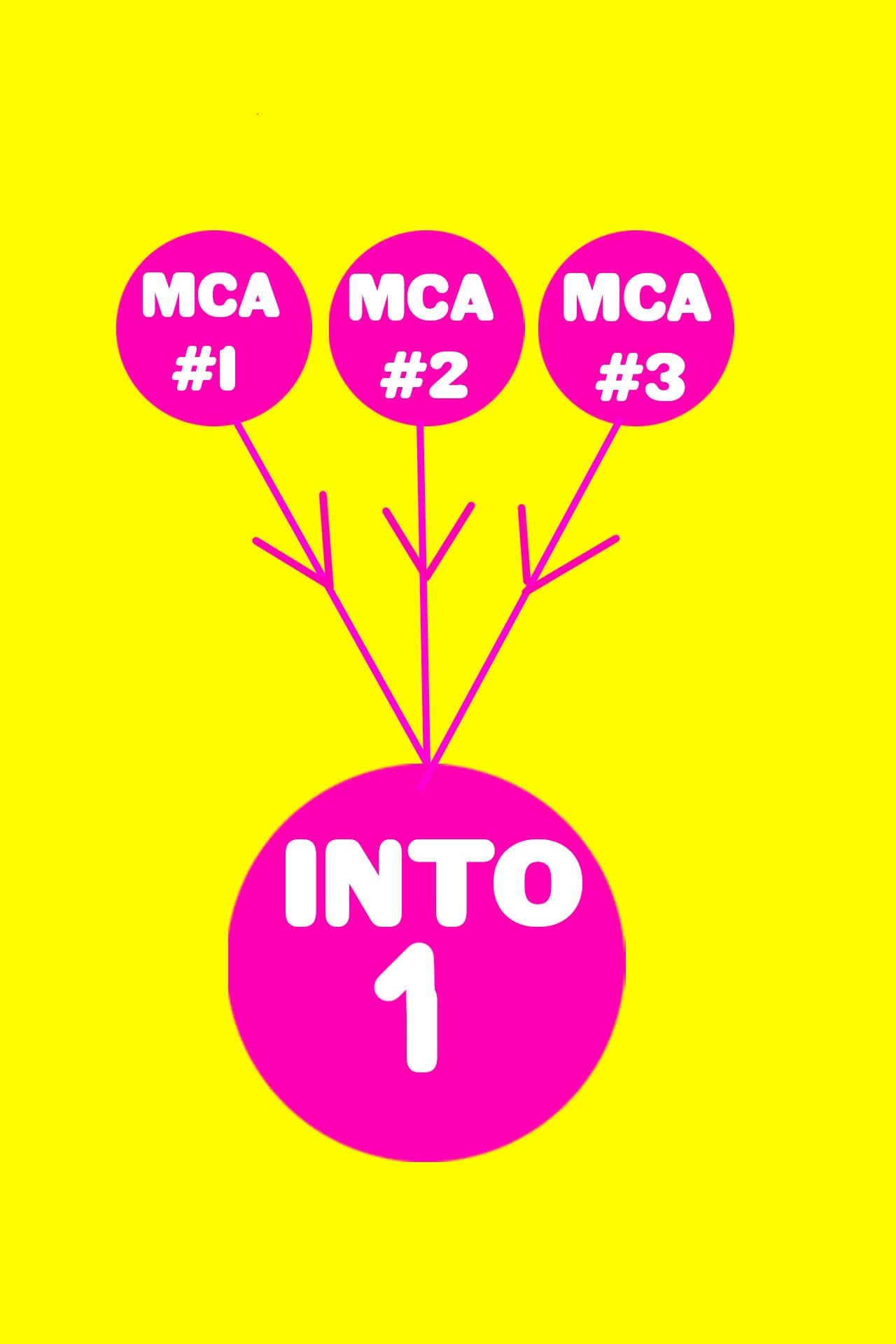

The best ways to consolidate merchant cash advances. These ways will not harm your business. No defaults and no closing your checking account. Several options to consolidate into 1 payment with a monthly payment.

The best and safe options to consolidate merchant cash advances. Many businesses have multiple mca’s by stacking cash advances.

Get immediate relief to lower their daily and weekly payments.

A regular and reverse consolidation will improve your cash flow up to 50% or more for some programs, thereby reducing your number of positions Apply below now!

Calculate how much you can afford to pay per day, week and month compared to what you are paying now.

Research and contact companies that offer consolidation programs that match your business needs and daily budget.

Review the qualification requirements and choose from programs that you have the best chance to qualify for.

Do not get another mca during the term of the transaction.

Why Not Consolidate Several…..Into 1 AND Lower Your Payment ?

FAQ Frequently asked questions.

How much can I save daily?

Your business can lower the daily or weekly payments between 25% and 50%. Some programs can lower them as much as 75% and convert into weekly or monthly debits.

How does the consolidation work?

A merchant cash advance consolidation is usually one large loan used to payoff several smaller ones. The goal is to lower total daily payments by extending the term, lowering the rate, or both. Some programs are structured differently or give you a longer term to payoff the current debt while others have a shorter term.

How do we qualify?

If you can simply make the new payment, then you can qualify based on cash flow. It should be 30 days since your most recent advance closed and you should be current. Lenders want to know you can meet your obligations now before being approved.

How can I get the best terms?

Apply for the longest term program available because the payment will be the lowest. The lower the payment, the more likely your cash flow will qualify.

How does a reverse consolidation work?

A reverse consolidation covers the payments on your existing advances while you make a much lower one on the reverse. During the term of the transaction, the other daily debits you had before drop off until you only have one payment left.

How we can help

Your business may be in a position where it must extend out the term of current positions. We can assist in paying off 2, 3 or 4 other mca’s and lowing your payment as much as 50% or more.

Tips on how to get approved:

– Make all of your payments on time.

– Wait until 30 days after the most mca closes to apply. Most requests are declined if new funding is deposited into your account in the last 30 days.

Lenders want to see how a business is paying it’s most recent debt before it approves.

– Don’t have more than 5 overdrafts or 5 NSF’s per month.

Program Features:

– No net funding requirement.

– No maximum number of positions.

– Daily, weekly, bi-weekly, and monthly repayment programs.

We try to tie payment frequency to your deposit volume. The main things looked at are:

The repayment history on current advances.

– If we are materially cheaper, and if your business has been able to pay your existing higher cost mca’s with minimal NSFs, we will aggressively pursue a consolidation.

– Deposit volume and consistency are reviewed. Are your deposits enough? Or are they under $10,000 a month?

If deposits vary significantly from month to month, we will typically look at the lowest month when calculating an amount to offer.

Up to 1.25 times your deposits with a 6 to 12 month term are offered.

– (NSF) insufficient funds and overdraft frequency are looked at.

Other features and products:

1. Advances are available in almost all states EXCEPT California. Term loans are available.

2. Your future consolidation is more like a like of credit. A merchant can request additional capital at anytime from us.

We will quickly re-underwrite it with no fee and offer additional funds and keep your scheduled payment the same.

Renewals

You do not have to pay off our loan to get more capital. This holds true if your business requests more capital after one month, or after six months.

Your business saves money at renewal. Your business will not pay interest on interest if you renew for premium programs.

– Low or no origination and underwriting fees. Fees as low as $250 to consolidate 3 to 4 positions, $500 to $750 for 5 or more. No NSF fees or other junk fees are charged.

– The maximum initial funding is $100,000.

– This is first position funding only. This funding can be the only funding following a consolidation. A standard line of credit, credit card split loan, traditional bank loan.

– SBA loan, car loan, student loans and home loans can be left in place.

– Daily, weekly, bi-weekly, and monthly payment options are available.

Your business may need help creating a business plan. The SBA can also assist with ideas and programs to develop a business plan.

Program # 1: Business funding based on the assets of the business. If the business has over $10,000 per month in sales, they may be able to get a business loan based on their sales.

Commercial real estate with equity can also be used to payoff the open tax lien. At closing the tax lien is paid off from the proceeds of the loan. Another option is to use business equipment. Get capital based on business equipment. Use the funds to payoff the tax lien. These options can also be used to pay a tax lien that has a payment plan and also tax extension deadline balances.

Business loans with an IRS payment plan

There are several business loans that can be obtained for a business with an IRS tax lien that has a payment plan. A business can use the revenues of the business or the hard assets of the business. This can be Real Estate or Equipment.

Business loans without a payment arrangement with the IRs.

A business that has a tax lien without a repayment plan can be financed. Businesses needing immediate help can now quickly use their revenues or assets to get working capital or a business loan. The process is fast and easy. Up to 5 to 10 business days and just a one page application.

Resolve your open business tax liens with several quick programs.

Finally, other sources of information related to tax liens may be found at the SBA small business administration site.

FAQ on business and open tax liens

What is an open tax lien?

An open tax lien is a lien that has been filed by the irs or state government against a person or business that does not yet have a payment plan approved for repayment.

Can I get a business loan with a tax lien on my credit bureau?

There are several business loan options for businesses with a tax lien or open tax lien that are usually paid off at closing. Options are based on assets such as real estate or equipment as well as on cash flow.

Do I need an offer in compromise from the IRS before I can get a business loan?

A formal oic is usually, but not always needed. Real estate or equipment backed transactions may allow for payoffs of irs or state liens at closing. Smaller tax liens may not require an offer in compromise to close a business loan.

How do I know if I have a tax lien against me or my business?

Registered letters are sent by the IRS and state when liens are filed against you or your business. It will also appear on your credit bureau and against real estate you own. The county real estate office will have a record of liens against property.

Should I pay a tax lien if it has already been filed and damaged my credit?

Most lenders will not approve a personal or business loan with an active tax lien. Companies and vendors you do business with may be reluctant to enter into a contract with one on your credit file. The IRS also has the power to seize any of your assets without notice.

Get money on your Truck, semi-trailer, dump truck or business vehicle now!

Video Description: Get a loan on a Truck, Van, or Car owned by your business. Get monthly payments. Truck can be in the repair shop now.

Get a loan on your truck and any other business vehicle. You can get up to $200,000 against Trucks that stay with you! Fast process and quick offers. Credit scores as low as 500. Need a larger loan for your Trucking Company? Visit our Trucking Company Loan page. Author Biography: Will Sanio

Get a loan on a Truck, now. Do you own it outright ? Then get money against your company vehicles, fast. Pick up trucks, Ford F-Series, Dually Dodge, Chevy, Box trucks, Semi-trucks, FreightLiner, Peterbilt, International, Dump Trucks, Delivery, and Vans. Low, and very low credit scores can work. To visit just the video page, visit Loan on a Truck Video

Watch: Trucks in action Video top of page! Click or tap arrow to play. Apply: Commercial truck title loans below now, or call 919-771-4177. Transcript here

Top 7 vehicles to get a business loan against

1 Commercial Vehicles

2 OTR Over the road trailers

3 Big Rigs

4 Semi Trucks

5 Dump Trucks

6 Trailers

7 Vans

Get a loan on a Truck, now. Do you own it outright ? Then get money against the Truck, fast. Even more, very low credit scores will work.

If your business has vehicles and needs capital, it can get a loan against tractor trailers, semi trucks, Vans, Dump Trucks or any business or commercial vehicle. Even 1 semi trailer truck can be enough to get capital. Loan amounts starting as low as 2,000 and up. Have a trailer? The add more funds with our loan on a trailer program.

Is your Truck or Rig down and in the shop for repair and the bill is more than you can pay? Get money specifically for a repair through a truck repair loan on a Big Rig or Truck that you cannot drive and is being worked on right now. This program will get your truck out of the shop and back on the road to let you make money again.

We have several premiere loan programs to get semi-trailer truck financing and credit scores can be lower under this program. Credit scores below 500 considered. The truck or semi-truck has to be free and clear collateral.

To get a loan to acquire trucks and trailers, try the hot shot truck loan program.

How to get a loan on a semi truck trailer, big rig or business vehicle: How to steps, direction, and tips:

How to get a loan on semi-trucks, tractor trailers and business vehicles

Estimated Cost: $0

Total Time: 1 Day

Supplies Needed: Semi truck trailer or business vehicle, title, picture of semi truck and odometer. Time available.

Tools needed: Internet connection, phone, computer

Step 1: Preparation

Research companies that offer loans against semi trucks, big rigs, dump trucks, or 18 wheelers. Search for programs that best match your business need for the amount needed, the value of your semi rigs, and credit.

Search for a program that offers loans on vehicles specifically of this type, including OTR Over the road trucks and trailers

Step 2: Have your information on your big rig semi trucks ready to go. Have a list of the value of your vehicles.

Tip: Start the process a few days before needing funding. You may need to get together information you were not expecting to get.

Remember that regular business vehicles such as vans may also qualify.

Information on the trucks you will need includes manufacturer, year, model number, title, a picture of the odometer and a couple of

pictures of your truck.

Have the information ready that you will be asked for such as the title, year, manufacturer and model number.

Step 3: Settle on the top 2 or 3 programs that best matches the value of the semi trucks you have and the amount you need.

Contact qualifying companies and ask about their approval requirements.

Tell the lender the basic information on the trucks and try to find out what your chances of approval are. Also ask if you can be pre qualified.

Call the lenders and ask about what is required for approvals and if you can be pre-qualified

Step 4: Submit an application

Apply with the program that can most likely get your business a loan against your semi trucks based on the conversations you had with the lender and review of their criteria. Complete an application for funding and provide the supporting items such as copy of the title, pictures and odometer reading.

When you have picked the most likely program, apply and submit your application information

Step 5: Review approval offers

After approval, review all closing terms and conditions. Make sure you can provide required closing items. Complete transaction and receive funding.

If you were declined, contact the lender and try to find out why. Try to find out if you are able to do anything to get the decision reversed and get approved. If you cannot get approved, then go back to the other lenders you looked at during your search. Ask if the reason for your decline will be a decline reason for them. If not, then consider applying with one of the other lenders.

Review the terms and closing requirements of any offer received. Pick the best one, provide the closing documentation needed and receive funds for your business.

If you have many vehicles as a used car dealer, consider options under our used car dealer loans.

Show Video Transcript

Loan on a Truck

Mike drives a Kick [beep ] Truck! But fuel prices, repairs, and tires were high, and going up !

So he called us and we got him money with a loan on a truck. Get Money against any Truck. Ford F-Series, Dodge, dually, Semi Truck, delivery, box and cargo, over the road heavy haulers, dump trucks and many more. Low credit scores OK. Do you own that truck? Find out how much money you can get today. Apply at SmallBusinessLoansDepot.com, or Call: 919-771-4177.

FAQ on how to get a loan on a semi-trailer, truck or business vehicle

Can I get money against my semi-trailer?

Yes. Your paid off semi-trailer, tractor-trailer, big rig, 18 wheeler, dump truck or business vehicle can qualify. You have to prove ownership of the vehicle and have the title. It must be in your possession or in the shop. For smaller cars and trucks, the business name should be listed on the vehicle and used mostly for business.

How much can I get?

You can get about 40% to 50% of the retail value. This is close to the wholesale or auction value. You can also use the Truck as collateral to make it easier to get financing to buy another rig.

Can I get money against my broken down semi-trailer to pay for repairs?

You can get money against a semi-trailer, Truck or other vehicle types in the shop to pay for repairs for transmission, body work, mechanical or other breakdowns. The shop will be paid directly to get your big rig back on the road asap. If the repair cost is less than the loan, then you will get the difference paid to you in cash.

Recent Customer requests

Recently, the owner of a single rig trucking company called and said his truck went down and was in the shop. The customer needed $6,700 for repairs and his credit score was mid 500’s. He wanted to get funds against his Semi-Truck. The truck has a value of approximately $25,000. He still owed about $16,000 on it and as a result, we referred him to another loan product because the semi-truck has to be free and clear.

A company should make up a list and provide it to the lender to get a loan against 18-wheelers. Offering multiple trucks is also another way to get more money. The trucks have to be free and clear. The terms the customer can get are usually attractive because they are not short term and the collateral is valuable, so the lenders will give more attractive rates. Customers can get a decision within one business day and close within a week.

Click on the contact link and get more information.

Get a loan on a semi-trailer truck, big rig, or tractor fast and easy. Monthly payment loans start at $2,000. Damaged credit and scores 500 and below are O.K.

Loan amounts:

Loan amounts are based on roughly 2 to 1 collateral and also on the wholesale value. Businesses with 2 semi-trucks worth $100,000 for example, will get an offer in the $40,000 to $50,000 range.

Online resources include an interest calculator. Customers can type in the loan amount, the number of months and the monthly payment to find out the interest rate.

For example, on a loan for $100,000 for 60 months with a payment of $2,163, the interest rate calculates to 10.77% and a total repay of $129,780.

Additional collateral is not required. A site inspection is normally completed before closing.

Tip: The trucks must be accessible and in working order. A UCC filing is placed with the department of motor vehicles in the state the business resides in.

Thank your for visiting our loan against tractor trailer page. The success of your business is our goal.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank headquartered in Winston-Salem, North Carolina, and First Atlanta Bank in Atlanta, GA. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

The Best Expertise for the specific Business Loan you want

Do you need help getting a business loan? If you and your business has experienced going to traditional banks or alternative lenders and not fitting into one of their programs we have some options and free counseling. Find solutions, learn and understand which programs are best to help getting a business loan for your business.

Options for help getting a business loan include options based on assets such as equipment assets, and based on just the sales of your business.

We will discuss your company’s particular situation and needs. We will help you determine what the best funding options are for your business. Once that is identified, we will help you get together any paperwork you need for that program and get you started.

Most businesses have the easiest time qualifying for either the loan against assets or loan using bank statements.

Many businesses that have been denied financing due to either unacceptable credit, collateral or financial statements have complained that if they have significant sales, so why can’t they get funding against their sales? We agree. We have assistance programs that provide help “getting a business loan” through just your company’s revenues or equipment. The funding functions similar to a business line of credit. The approval is based mostly on the business’s total monthly deposits, average daily balance and time in business.

We will provide help getting a business loan by assisting your business with the processing. Just provide your most recent 3 months complete business checking account statements and a short one page mini-app. Other ease of program include:

Fast and easy processing

No financial statements to provide

Easy personal credit and time in business requirements

Quick funding through a wire into the business checking account

within one to two business days.

Approvals are up to 125% of the total monthly deposits. If a business deposits $50,000 per month, the business may qualify for up to $62,500. The amount they will qualify for will depend further on the time in business and average daily balance. Terms are between

3 and 18 months, while most approvals are for 6 and 9 months. The customer can borrow and repay repeatedly. Once the customer pays the original balance down to about 40% of the original balance, they can borrow against the line again. The best way for help getting a business loan is to get the assistance of an experienced representative. Early payoff is limited and the customer will not get much of a discount.

We need to talk about time in business. The business only needs to be operating for 9 months, though any time in business more than 2 years means you will have more of a chance of being approved and increase the approval amount. All other things equal, a business that has been in business for 3 years will get higher approvals than a business that has been in business for only 6 months.

There are more choices for help getting a business loan through the loan against assets program. A business can get working capital using either their computer electronic equipment, machinery, industrial equipment, construction equipment, dental equipment or medical equipment. Loan sizes are from $10,000 to $250,000, with just an application only for most cases up to $40,000. The business just provides a one page application and equipment list. Up to 75% of the current value of the equipment can be obtained.

Terms:

Terms are 24, 36, 48, or 60 months. There are early payoff options, although they are not favorable or give a large discount for early payoff. The funding is set up either as a lease or an equipment finance agreement. Leases are designed to provide the biggest deductions but are not the best for early payoff.

Sample transaction in which a business received help getting a business loan.

Sparks Engineering needs $50,000 in working capital. They complete a one page application and equipment list. The list includes technical equipment such as measuring instruments as well as computer equipment, including Servers, technical engineering software and hardware.

Their bank statements show they are depositing an average of $60,000 per month. They are approved for $30,000 on a loan based on bank statements and $30,000 on a loan against their equipment. The $30,000 loan based on bank statements is for 9 months. The loan against equipment can be done for 24 to 60 months. Sparks Engineering does not want to have the entire $50,000 financed for only 9 months because the monthly repayment would be too high. They decide to take $20,000 with a 9 month term and $30,000 with a 36 month term.

Both sets of documents are E-Mailed to the customer. They complete and return the docs. After the docs are checked for accuracy, a decisionlogic bank verification and final verbal verification is completed with the customer. Once the customer confirms the transaction, funds are wired into their account within 24 to 48 hours.

FAQ’s:

Most frequent Requests:

– I need a business loan.

– Get me a business loan.

– Help me get a business loan.

Some customers call in, skip the questions, and just ask us to do consolidate advances. All of these requests fall into the same MCA consolidation relief product.

Question: How much of a loan can we get?

Answer: The amount depends mostly on the amount of your business’s sales, the amount of equipment the business has, the time in business, and the credit.

“Credit Inquiries” has been a topic of much conversation and concern in recent years. The following is current information you should know about credit inquiries you may not want to avoid.

There are however, credit inquires you should not avoid because they often are the best programs available in the market. Soft pull credit options are available as well. Apply Below:

Some of the best business loan programs are hard pulls

Avoid all credit inquiries can keep you from getting what you want..

Many people are reluctant to have credit inquiries to be pulled on them even if they are applying for a loan. They tell lenders that they want to be considered for the financing without their bureau being pulled.

This is not feasible or realistic, especially if the request is in the name of an individual. In most of these cases, these requests are in the name of a small business and the owner wants the request to be in the company name, not in their personal name.

If a business has less than 35 employees, in most cases the lender requires the owner’s credit to be reviewed. There are options you can take if you have had too many credit inquiries pulled.

But I pulled my own credit report!

Virtually no lenders will decide your loan request with a consumer obtained bureau.

Consumers can contact credit reporting agencies as well as outside vendors that provide bureaus and get all 3 bureau reports. These files are not the same that lenders obtain. Consumer reports are formatted differently and are simpler than the lender’s re. The consumer version often provides more written explanation and sometimes less numerical detail.

Consumers will sometimes review their bureau and tell the lenders to use the consumer obtained reports they have rather than the version pulled by the funding source. The report the consumer has will almost always be older. The lender wants to see if anything has happened since the date of the report the consumer has in hand.

There are many outside vendors that provide intermediate party credit files. Lenders are not, and should not be expected to know whether those vendors provide updated and satisfactory information. Lenders are not obligated to use those. As a result, consumers should not expect to avoid inquires by demanding that lenders use their consumer version.

Determine what your balance is. Complete a list of your equipment assets, which includes Computer, medical, industrial equipment and machinery.

We will approve a loan to payoff your balance and payoff or reduce the number of cash advances. We will also help you set up a 24, 36 or 48 month repayment term. Even if you only want to term the balance off to 24 installments, this will significantly improve your company’s cash position immediately.

Payoff Examples

If you took out a $25,000 merchant advance for 6 months, then you were paying around $248 per day, or $5,457 every 30 days.

By terming the financing out to 24 installments, you will reduce the payment to $1,562, which is only 28% of what you were paying. If you go out 36, you will reduce it to $1,083, or 19.8% of the original amount. This difference will make a dramatic positive influence on your cash flow.

Most frequent Requests:

– Help me payoff my MCA.

– I need get rid of my MCA Merchant Cash Advances

Help my business get out of my cash advances.

All of these requests fall into the same MCA consolidation relief product.

Example:

Tucson belt company pays off merchant cash advance with 1 loan.

Tucson belt had 3 merchant cash advances totaling $75,000 with a total monthly payment of $15,000. This burden was killing their cash flow. They had 6 months left on their advances. The three advances were combined for 1 loan for year.

The monthly payment was lowered to $7,500, thereby increasing the company’s cash by $7,500. President Bradford Jennings told BizTucson, “This Consolidation program was an excellent and necessary way to improve the cash flow for these Advances. It has dramatically improved our financial standing. We will be able to increase our advertising and inventory levels. Gross receipts are expected to increase and net income rise. We look forward to using the increased funds for expansion.”

If you are a business owner that took out a short term cash advance and are saying any of the following things or questions below, contact us today to get instant relief.

Most callers say they need to urgently get out of a merchant advance. Many companies tell us they can’t handle it much longer and feel trapped.

You will only need to complete a short 1 page Mini app and provide an equipment list which can be completed online. The approval process takes 1 – 3 days. If you are approved, the closing documents may be E-Mailed to you or completed online. You complete them and return the completed documents via fax. A verbal verification call is completed with you and you receive funding within 1 to 2 ays afterwards.

Video Description: Get out of an mca. Several options for businesses that cannot handle their current cash advance payments. Refinance and extend the term. Options to lower the payment 25% to 50% without being reported as late or defaulting. Avoids, and is not the debt settlement option that still defaults customers after they pay thousands and very little or nothing is done.

How do I get out of my merchant cash advance?

Get out of a Merchant Cash Advance (Video Transcript: Click to Expand)

[ city street noises ] welcome to smallbusinessloansdepot. [ young woman says Ooh! ] Do you have a merchant cash advance that is

causing your business a monthly cash flow situation that is far more difficult than you anticipated?

Get out of MCA: Options

We have several flexible programs and are specialists in either retiring or extending the term from your current 3, 6, 9, or 12 month merchant cash advance term, and terming it out, 12, 24, 36, or 48 months. Start the process by clicking on the application or website link in the description below. Please like, subscribe and share.

Not a debt settlement option

This is not a debt settlement option or company where you are made to pay thousands of dollars, wait months while the debt settlement company [ woman says no ] does very little or nothing and you still default on your cash advances and debt anyway and your business gets reported to the default databases. Contact us today direct at 919-771-4177 and we will take this merchant cash advance and term it out and retire it and get you out of the difficult cash flow situation.

Examples: Payment Reduction

We have taken business, many, that have $4,000 a month and lowered it to $750 a month. Take $3,000, lower it to $600 a month. Take the cash flow. Free the monthly cash flow and use it for other critical needs you have today that you have to address with your business. We are specialists in this program. Let us retire and get you out of the merchant cash advance syndrome. Call us at Tel: 919-771-4177 or go to smallbusinessloansdepot.com. On YouTube, please subscribe, like and share.

Many businesses have taken out short term advances against their future sales. Stop your crushing merchant cash advance nightmare immediately and permanently.

There are several program options to eliminate advances, for instance, a payoff, consolidation and also asset based programs and more. Get your freedom and business back. Apply now, below: Author biography: Will Sanio

How do I get out of my mca merchant cash advance?:

Search online for programs that will help you exit your merchant cash advances without defaulting or having problems with your existing merchant cash advance companies. Also look at any reviews

Programs that will payoff your other advances while you pay a consolidation or business loan will be the best option. For example, settlement programs are usually not the best choice.

Review the features and benefits of different cash advance consolidation relief programs so you can make sure they apply to your business.

Read the features and benefits of each mca cash advance consolidation and relief program.

Pick the program that you feel is the best match to get your business safe from your cash advances and discuss the program details with the representative.

Select the program that you think is the best one to payoff your cash advances and keep your business open

Apply. If approved then review terms and closing stipulations. If the new terms put your business in a cash flow position that will allow you to stay in business you can consider closing the transaction.

Review terms and closing conditions. If the cash flow will help you stay in business consider closing the transaction. Review the closing conditions to get all the items needed to fund the transaction. This may include payoff letters from your current mca merchant cash advance companies. Determine the payoff for several days in advance.

When closing get all items needed to meet the closing conditions. For example, this may include payoff letters from your current mca merchant cash advance companies. Also get the payoff for a few days into the future.

We are a leading funding source for all Small Businesses looking for the best alternatives to Banks.

Author Biography:Will Sanio, Owner of SCF Funding, dba SmallBusinessLoansDepot.com, has a Bachelor of Science Degree in Business Administration with a concentration in Finance from the University of Tennessee, Knoxville.

Over 20 Years experience including 10 Years with Wells Fargo, formerly Wachovia Bank and First Atlanta Bank. Specializing in Traditional and Alternative lending.

Will Sanio: University of Tennessee Diploma – Bachelor of Science in Business Administration with concentration in Finance – Click or Tap to Enlarge Image.

FAQ Frequently asked questions on how to get out of a merchant cash advance.

How do I get out of my merchant cash advance?

The programs combine one or more advances into one loan and extend the term. It will improve your cash flow and not involve settlements or negotiations to lower payments. Your current advance companies will not be contacted and your credit will not be impacted.

Are there longer term options?

Terms are available up to 24, 36, or 48 months and longer in many cases. Businesses can take out an asset based loan against their main assets or a revenue based solution. Businesses cut their payments an average of 50% or more.

Can I get emergency cash to save my business?

Yes. Programs are available to allow your business to get instant relief from suffocating advances taking too much out of your account. Your business cash use the cash for basic needs such as payroll, utilities, rent, and inventory.

Can I get out of my cash advance and also get cash?

Your business cash flow will be reviewed. If the business can handle the new payment, it can be approved for a refinance plus cash.

How fast can I get out of my merchant cash advances?</strong

Processing time from application to funding is 2 to 3 business days and can be as fast as the same day. If you apply and immediately complete closing documents, it is possible to get funding within 24 hours.

Can I declare bankruptcy on my cash advances?

Bankruptcy is normally a filing on all or specific creditors rather than just merchant cash advances. You may still be required to make monthly payments during bankruptcy. Contact a bankruptcy attorney to get detailed information about your options

Can I stop payment on my mca merchant cash advances?

It is very much not recommended to ask your bank to put a stop payment on the daily or weekly payments. It may be considered an intentional default by mca cash advance companies. Significant default fees and penalties apply and advance companies will often seek a judgement against you if you stop payment on their daily debits. A better solution is to negotiate a payment you can handle.

Are there state or federal laws that protect me from merchant cash advances?

There generally are no state or federal laws to protect you specifically from mca merchant cash advances. However, compare any questionable contract terms to existing laws and seek legal advice if needed.

Other frequent requests for assistance:

– Help me save my business.

– I have a problem and need to escape my merchant cash advances.

– I need to stop my merchant cash advances.

Many customers don’t ask questions just and say they need to be rescued from their advance emergency immediately.

– I have a problem paying my mca’s.

Most common requests and comments by callers:

I need emergency cash flow right away. Most callers say they need immediate cash flow. Some callers still have signifiant cash flow and say they need another advance asap.

1) These cash advances are destroying and ruining my life and my business.

2) I am suffocating from my merchant cash advances and need to lower my merchant cash advance payments. Also, I need emergency funds right now.

4) My merchant cash advance payments are killing me, so I can’t sleep and am also having night mares from what these cash advances

are doing to me. Merchant cash advances are strangling my business cash flow.

Are you asking yourself why the bank declined my business loan?

Where can you be approved? Helpful tips to turn a decline into an approval and find other business loans. Match your business to small business loans that you will get approved for !

What caused my business to be declined and what are the most common decline reasons Common reasons are:

If you have been turned down for any decline reason, contact us. We specialize in difficult to approve businesses and business loans and have programs that can approve your business for any decline reason.

If you think the bank declined my business loan for wrong reasons, then the first step is to call up the company that turned you down.

Determine if you are speaking with someone that has the knowledge and experience to provide you with useful information about the decline. If you received a letter, call and confirm the decline reasons.

For more information on strategic reasons, read why banks don’t lend to small business.

Reasons why your business loan was declined

FAQ Frequently asked questions on why the bank declined my business loan

Why don’t banks lend to small businesses?

A high percent of small businesses fail in the first 5 years, so they are considered a higher risk than larger businesses. A small business has to have excellent personal and business credit, strong collateral and financial statements to get approved at a bank. In most cases only certain collateral is accepted that can be easily liquidated with a value between 200% and 1000% of the amount of the loan. Financial statements must show steady or increasing gross profit and net income.

Are there alternatives to banks for business loans?

You can successfully get a business loan by understanding the different alternatives available in the marketplace. Then understand what it takes to get approved and the reasons you may be declined. Understand the strengths and weaknesses of your business and apply for the best matching program.

What can I do after the bank declines my business loan?

Ask a loan officer to discuss all of the decline reasons. Also ask how you can correct those to get an approval and if there were any other concerns. Get information as specific as possible and consider alternative business loans while you are working on the bank’s decline reasons.

More info on why the bank declined your business loan

Missed daily payments

You have an existing daily or weekly Merchant Cash Advance and you have missed payments on the advance. Missing daily payments is a major reason why a new loan request may be denied. Missed daily loan payments may can a renewal request to be denied.

Average Daily Balances too low

This decline reason means that your daily ending balances were too low over the month. Lenders have different balances that they want

and often will not tell you. Many lenders often want at least $1,000 Average Daily Balance consistently in your account.

Inconsistent Cash Flow

Business cash flow has fluctuated too much from month to month. In some months the cash flow meets the minimum required by the program and in other months it does not.

Declining Cash Flow

Total monthly deposits into the account have been declining month to month from recent low sales. Even if the average still meets criteria, the lender may still feel this is a reason for the turndown.

Does not meet criteria

This is a general decline reason. the lender does not want to tell you what this means

Month to Date MTD

This a decline reason that often happens with Merchant Cash Advances. The Month to Date activity is requested for the current month and the approval be declined or reduced when current months deposits are lower than the previous three months.

Ask if significantly lowering the amount of the request, adding a strong co-signer, or adding more collateral would cause them to reconsider and possibly approve the application. Speak directly with the credit department that makes the credit decision.

If any of the reasons you are declined for a business loan involve credit, you will want to contact at least one of the credit reporting agencies to determine what is on your credit file. You may already know most of what is on your file, though you should get a copy of your file to confirm it.

If there are any inaccuracies, you should dispute them with the bureau. This is easy to do and can improve your bureau without significant effort. You will succeed in getting derogatory information removed when the bureaus cannot prove the derogatory reporting is accurate.

Once you accept what is on your credit report, begin looking for other alternative loan options. First determine what are the strengths of your business and weaknesses of your business. When you contact companies, find out as much as you can about what their alternative loan options are based on.

Instead of choosing the business loans you like best, organize the loan types in terms of what your business is most likely to qualify for. Of those loan options, then decide which ones you believe you should proceed on.

Other Loan Options

Discuss the loan options with the representative and speak with someone who is knowledgeable, rather than someone reading from a script. If they don’t give you logical answers to your thoughts or concerns, try to speak with someone else. Don’t feel that you must get all the funds you need through 1 type of loan, or all of it immediately at that time. There may be 2 loan types that you should proceed on.

If your business needs $100,000 in total, and you only qualify for $50,000, this may still work by getting the funding in segments over time. You can take the $50,000 you qualified for and also work on getting the rest of the funding required over the course of the next few weeks or months. Chances are you did not need the entire $100,000 immediately. Most businesses that receive $100,000 do not spend it all within the first 30 days. These steps are important when your business has been declined.

For additional resources to help you prepare for future business loan requests, you can

also visit the SBA. The SBA government site has numerous resources which can assist your business.

Thank you for visiting our resource page on what to do if you are declined for a business loan.

In most cases, a business line of credit is the most difficult type of financing to get. Business owners should look at the terms. This includes interest rates, number of months, total amount of the repay, and early payoff considerations.

FAQ Frequently asked questions on how to get a business line of credit

How can I get a business line of credit?

Time in business of two to three years is often required. Other requirements include a 680 or higher credit bureau score, full financials and industry requirements. Full financials means 3 years business and personal tax returns, a personal financial statement and interim financials. Interim financials are a year to date profit and loss statement and balance sheet.

Why are business lines of credit so difficult to get?

A business line of credit is hard to get because it is set up to be available indefinitely to the borrower and does not have a limited term. Lenders consider this long term exposure to be high risk and require a longer history of business success with increasing gross and net income. If the business shows low net income and flat revenues, they are unlikely to be approved for a business line of credit.

Can my lender require me to suddenly payoff my business line of credit?

An annual payout provision and the lender being able to call the loan and require payoff at anytime is legal and enforceable when it is written into the contract. These provisions are extremely risky for borrowers. Lenders sometimes call loans because they decide to lower their risk models, or when they are being acquired by another lender. They may call loans even if the borrower has a clean payment history. Borrowers do not know in advance their loan is going to be called and often cannot pay it off immediately. Their business could fail because lenders may be able to seize their accounts receivables, real estate or any other collateral attached to the line of credit.

Some lenders put conditions on a line of credit that negates all of the other advantages of the financing. Lenders may require the borrower to put up their home as collateral. Borrowers should realize this becomes a home equity line of credit. Borrowers are then giving their home and business assets as collateral. Why not not consider a home equity line of credit then?

Borrowers may be better off looking for other financing first. Attempt to negotiate the terms of the approval with the lender when your business is using real estate as collateral.

In most cases, banks are the institutions that require annual payout provisions on business loans.

The balance has to be paid down to zero at least once per year. This is a major negative that borrowers should be very cautious about.

Don’t mistake this for a minor aspect of the transaction because it could end up being very hard for the companies to do. Very few can payoff a balance on any debt once per year.

Borrower considerations

If an annual payout provision is not met, what can the lender do? If the company does not pay the balance off once per year, the lender may have the right to:

Call the loan due and to be paid in full immediately or face a declaration of default.

Raise the interest rate

Impose heavy penalties and fees.

Do they have the right to take some or all of the collateral? Can they liquidate any listed stock or bonds that were pledged? If so, how likely is it the lender may do this?

Will the lender liquidate assets fast or only if the borrower goes very far past due? These questions need to be asked. Borrower that pledged free and clear collateral such as real estate as security may have high risk exposure.

The borrower needs to consider the requirements if real estate is secured for the transaction. For transactions larger than $100,000 or more, the borrower must closely monitor their cash flow during the year.

Even for businesses that have high annual sales, coming up with a significant amount each year is challenging.

Consider your average monthly bank balance as an estimate of the most they can come up with to meet an annual payout provision. That amount is the maximum balance they should carry on their loan during the year.

There is a simple way to get a 10% increase in an approved loan without having to qualify for it. Just ask for an increase in the approval and ask for an amount that equals a 10% increase. Apply below for loans that offer the easiest bump in the approval amount.

How to get an increase in your business loan approval amount

Step 1 Tell the lender that you need an amount that equals between 5% to 10% more than what your business was approved for

Step 2 Provide any supporting information you may not have provided before that gets you a better business loan offer. This can include tax returns, additional bank statements, financial statements, personal financial statements or other items.

Step 3 If approved, review any updated terms and close transaction

Step 4 If denied, ask why. Determine if you can satisfy any denial reasons

Apply for funding below.

Many loan programs allow for a 10% increase on a newly approved loan if either the credit representative or the customer simply asks for it. In many of these cases, credit is not pulled again, there is no additional review and a reason for the increase is not asked for.

Very few consumers are aware of this and do not take advantage of this. Such an increase is not advertised by lenders because they wish to approve what the customer asked for or the maximum they can qualify the customer for. They merely do this in the event a customer wants more, 10% is considered small enough to be within the risk parameters of the credit decision.

As an example, a customer applies for $50,000 and is approved. If the customer indicates they wish for more funding, they typically can get an additional $5,000 simply by asking for an increase. An automatic 10% increase is the limit, lenders will not stretch to a 20% increase without a further review or more information, possibly financial information being asked for.

For example, if a customer is approved for $50,000 and insists on $75,000, then further financial information may be asked for to consider the request, such as a Personal Financial Statement or Business or Personal returns. If the applicant can show just a small amount of other sources of income, that may satisfy an increase request. In some instances, providing the most recent 3 months business checking account statements is enough.

These are some of the ways in which a borrower can increase the amount of an approval.

Repossessing the assets are hard after a customer defaults.

Recovery may be impossible. Collateral located inside of another business may be hard to get back.

Vendors that need to finance customers: Example of challenges.

A bowling alley contracts with 1 company for vending machines and the machines are financed through a lender.

The customers defaults and the lender wants the machines back.

The lender hires an outside company to repossess the vendor’s machines. They show up at the bowling alley and the manager does not allow the machines to be removed.

Now the owner of the business has to be called to agree to the removal. If they do not agree, then the lender may have to take a loss on the loan.

The case can be taken to court, but this may cost the lender more than the assets are worth. Instead, they usually try to negotiate. When that fails, the loan is considered a loss.

These are some reasons why vendors have a hard time getting customers financed.

To get funding without a landlord waiver closing stipulation requirement, apply below.

Lenders require landlord waivers to avoid or minimize losses for businesses with bad credit or slow pay as well as default on previous loans. Many business loans include collateral that is on the premises of the borrower. The landlord waiver allows the lender to enter the property and obtain the collateral in the event of a default. If the lender did not have a signed landlord waiver, they could not enter the place of business of the borrower to take their collateral. Landlord contact information will be ask for if this is required.

Without the landlord waiver

The lender cannot legally enter and repossess collateral. The owner of the property can seek recourse against any lender entering the premises without permission of the landlord. There are some business loans in which a lender asks for a landlord waiver but does not consider it critical for the loan. This requirement is one of the top customer complaints with business loans.

A lender normally considers a landlord waiver absolutely critical if they ask for it and will not fund a transaction without the waiver. Lenders worry that a landlord will refuse to allow them on the business property. If this happens, the lender may not be able to recover their collateral if there is a default.

Why do I need to get a Landlord waiver?

Example: In the vending industry

Lenders that finance multiple vending machines will not fund transactions without all of the required landlord waivers. Lenders that finance vending machines know that if they finance 10 vending machines, those 10 machines may be in 10 different locations throughout a metropolitan area. If the borrower defaults, the lender would have to go to 10 locations to pick up the collateral. They also cannot simply show up at a place of business to pick up collateral. They must also have to have permission from the owner of the property because they will be uninstalling equipment, which is considered making a change to a property. The lessee agrees in the lease not to make a change in the property without the permission of the landlord, so the lessee must contact the landlord.

What is a landlord waiver? Are landlord waivers required for a business loan?

In the event of a default on this asset based loan lenders do not want to contact 10 different landlords. Each landlord would have to agree to an on site repossession. The landlords know if they agree, those business that leases space from them may go out of business.

The landlord does not want the lessee to go out of business. The landlord may want to deny the request.

These are the reasons why lenders will ask for this when a business loan is first closed.

The SBA also offers info on small business and negotiating with landlords.

Need a larger business loan and can’t qualify for one? Get it all in multiple business loan parts! Get several smaller loans to reach the total amount your business needs. Apply below now for programs designed for your business to get the total it needs.

A business needs $100,000 and cannot qualify for $100,000 in one loan. However, the business can qualify for approximately $35,000 so first obtains a $35,000 loan. After the first loan, it applies for a second funding and even a third round of funding. This strategy makes it much more likely for the business to raise the full capital it needs.

Many businesses do not use all of the funding in the first weeks. Many times, the business uses the funding over the course of weeks, and even months after closing. Some businesses may get $100,000 all at one time and use it over the course of 3 months. That is almost the same as if they had obtained the funding in 3 parts of $35,000 over 3 months. Restaurants often do build outs and spend the money over time instead of all at once.

FAQ Frequently asked questions on multiple loan parts

What does multiple loan parts mean?

Getting more than one loan as part of one effort. When a person or business cannot get approved for the entire amount they want in 1 loan, they get multiple parts until they get the full amount they want.

Why don’t I just ask the 1st lender to approve the total I want?

Each lender decides how much they are willing to approve your business for under their guidelines and risk model. A second or third lender may give you more funding because they are approving less and not taking on the total risk

themselves if there is a default.

Do I have to let each lender know how much I got from the other ones?

No. Each lender will see that you have a new account, had a recent inquiry, or

may check your recent back activity to see if you just got any new loans. They will ask about recent loans if needed.

Banks and similar lenders prefer lending to certain industries, such as Medical, professional and manufacturing. Does that mean that certain industries are at a disadvantage when applying for a business loan? Yes. Apply for programs that will approve loans in industries other lenders will deny.

In short, yes. Service industries, industries that are heavy in service and hospitality do not have some of the advantages that other industries such as Medical and manufacturing have. Service and hospitality industries generally do not have hard collateral which manufacturing and Medical have much more. Both medical and manufacturing both have valuable equipment which can be taken as collateral in a loan request.

Another advantage that the Medical, professional and manufacturing sectors have is that on the average, they stay in business longer than service and hospitality industries. Service industries such as Restaurants have a higher frequency of going out of business.

The past due rate for industries such as Medical is far lower than average in the loan portfolio. One of the reasons lenders like Medical practices is that their past due ratio and default ratio is among the lowest of any industry. It is also known in the lending industry that Restaurants go out of business more often than the average business. This results in a double negative for lenders. If a certain business sector goes out of business more frequently and they do not have collateral, then the lenders will lose more often lending to these sectors, and they will lose more money at the time. In summary, the lenders lose more money more often.

While Restaurant and certain hospitality organizations do have some collateral, Restaurant equipment and hospitality equipment such as beds and furnishings will bring in far less than production equipment and used medical equipment.

Lenders will not discuss these issues, however most traditional lenders do not favor certain service industries such as Restaurant, as well as hospitality industries.

There is a long history in credit of using a strong Co-signer to strengthen an application. However, can they make up for a bad credit primary applicant?

It is anyone that signs with you on a loan request. It is normally done when someone with stronger and better credit than you offers to sign to help you secure financing. A co-signer is jointly liable for what they are signing for.

In general, a strong Co-signer does not make up for a bad credit primary applicant. If the primary applicant has a lot of derogatory information, a strong co-applicant often can’t help turn a decline into an approval. Great credit does help in situations when the primary applicant is not strong enough, has limited credit or minor negatives on their bureau.

There are several reasons why a strong Co-signer is often not helpful when the primary signer has significant derogatory credit.

Lenders know that in most cases, Co-signers sign only to help the primary applicant get the loan. They really don’t want to pay past due or default payments.

Examples are parents that sign for their children to help them get a car loan. However, there are many other examples. Sometimes another relative or friend may help them get the loan. In these cases, the secondary signer does not get the proceeds or asset being applied for.

Due to this, if the primary applicant runs into difficulty and cannot repay, the guarantor usually does not want to pay because they received no benefit from it. In the past, guarantors have told lenders that they just signed the paperwork to help the other person get the loan.

In some cases, the C0-signer really believes they will not be held responsible. They believe their responsibility stopped after they signed the paperwork.

Lenders know primary applicants with bad credit will go past due often. As a result, the excellent credit guarantor will be asked to make good on the debt.

Strong Co-signers cannot always help a derogatory credit primary applicant get approved for a loan.

There are many reasons why changing your business name is necessary. It may be re-branding, expansion, or other good reasons. Maybe the business name was bad when the company was set up with the secretary of state. But it may also be for not good reasons, such as solving an image problem.

When it comes to financing, a name change is not a good idea and should be avoided. Even if the business can prove it is the same company and only the name was changed, this explanation has always been looked at warily by lenders. Often lenders see a name change as a new business.

If your business needs working capital such as a bank statement loan during the change, Apply below. Our programs are the most flexible available with the toughest credit options.

This hurts significantly in a financing request because if a company has been in business for 7 years, and changes the name in the last 2, it will almost look to a lender like the business is 2 years old.

Check your business credit report. If the business credit reports have the old company name, this will hurt.

If the business credit reports have the new company name and the business start date shows the full 9 years in business, this scenario will be penalized far less severely.

One answer would be to only somewhat change the business name, if possible.

Example

An example of large corporate name change for a bad reason was Valujet. Valujet suffered a major crash in the Florida Everglades in the late 1990’s and primarily for this reason, changed their name to Airtran.

A change from Alley Pizza to Back Alley Pizza is minor and not noticed by customers. If the name change is too much, then it sounds like a totally different company.

FAQ Frequently asked questions.

Will we have problems if we change our business name?

Existing customers may not recognize the new name of the business. You may also have to start an entirely new business with the secretary of state. This also causes your business to be totally new legally and the time in business under the old name stops.

I bought an existing business. Should I keep the old name?

Keeping the old name makes your name recognition and branding much easier. You can have the full time in business under the old name and the time in business of your new name. Getting loans and establishing business relationships will be easier.

What should I do if I have to change our business name?

Contact your existing customers and let them know what the new name of the business will be. Explain the reason for the change. Create marketing materials to use at your place of business for your current customers to see. Contact the Secretary of State and try to change the name of the existing business profile listing without creating a new profile.

Conclusion

Changing a business name has more drawbacks than advantages. Above all the business loses it’s main brand identity.

However, if it is a must, then prepare for all the consequences in advance, thereby minimizing the damage.

UCC blanket liens are when a lender places a lien on ALL of the assets of a business or a person at the Secretary of State.

Banks and other traditional financial institutions typically place blanket liens on a business loan. What do they cover, what restrictions do they cause companies?

Apply below now and instead get a business or personal loan without UCC Blanket liens, including unsecured options!

Several options, both unsecured and partially secured, are available. Do not let a lender take everything you have worked for just because your company runs into a short term cash flow problem!

UCC stands for Uniform Commercial Code and are against the specific property of a person or business. For example, blanket UCC liens are usually against all property, including furniture, fixtures, and equipment.

Details will vary based on the funding company. Investors making unsecured loans such as an mca cash advance won’t do this, though may still encumber accounts receivables.

Traditional funding sources such as banks will write in specific details, that may include:

It is a legal recorded by a lender with the secretary of state on an individual or business. It is legally binding and any listed assets are held as collateral by the filer of the lien.

What is a ucc blanket lien?

A blanket refers to a lien filed against all the property, furniture, fixtures and equipment that a borrower has. It means the lender has everything the borrower owns as collateral. In the event of a default, they can take court action to repossess and liquidate that property.

Can I get another loan while a lender has a ucc blanket lien on all of my assets?

Only unsecured loans are available to you until the lien is removed. If multiple assets were taken as collateral by the lender, you can request they release some of those assets. They can do this when most of the loan has been paid down.

How do I remove a UCC filing?

You can delete a ucc filing by paying off the debt or contract for which the UCC was placed. The lender usually files a release of lien automatically after the debt is fully paid. Check with them after the payoff to find out when they will release their ucc. If they have not, tell them to release it immediately and ask for a payoff letter. You can provide the payoff letter to the secretary of state and ask them to remove it.

Other Issues

Avoid liens on future assets. This happens when the company buys more assets during the loan. The existing finance company now has blanket rights to anything the company has bought outright.

Violations of UCC liens

There is another legal grey area even with a regular UCC blanket filing. Regular UCC blanket liens are on all property, furniture, fixtures and equipment.

If the company acquires property which a new lender takes as collateral, then there may be ownership conflict with that collateral.

Also, any new lender may not have a clear legal right to that asset based on the previous Uniform Commercial Code.

Finally, there are significant issues that come with collateral Uniform Commercial Code filings. Businesses should do due diligence or seek legal counsel.

Recently, some regular for profit companies have inquired how they can get free loan grants. Many Grants are not for profit companies, unless they fall into certain limited specific categories which sometimes change. For excellent alternatives to Grants, click below.

Complete the Data Secure 15 Second Request Form Now.. Click on “Paper Clip” attachment at bottom right and attach the last 3 months bank statements, or just complete Application.

Or, On Cell Phone, just tap either Tel # link, 1-919-771-4177, then Press Dial on your phone. You can Tap / Click Contact-Me, complete and we will contact you.

The public often believes that grants are available from the Government and do not have to be paid back. Grants are given mostly to non profit businesses. There are some exceptions that change over time. States may issue grants business in certain industries. For example, certain technical or scientific industries that government wants help from private industry in.

They sometimes states will issue Grants to certain businesses in the farming sector as States wish to promote the continued health of farming in their States. There are also instances in which certain minority owned businesses may be provided Grants. In general, For profit businesses do not receive Grants. Federal and State governments do not wish to provide money from revenues to businesses that are engaged in for profit endeavors.

Many new businesses that need a start up business loan look for help. They contact companies who advertise they can get grants for private companies. Many of these advertisements do not say that grants are mostly for non profit businesses. There are also many companies that advertise books as well as online books that are sold on how to obtain Grants. These fall into the same category in that these books are being sold on how to get something that in the vast majority of cases, does not exist.